Oracle Survey: Incumbent Banks Must Go Digital To Stay Relevant

by Fintech News Singapore April 20, 2018The era of traditional banking is coming to an end as customers are now demanding banking to be better integrated into their digital lifestyle, providing service that is instant, integrated with social platforms and driven by data, according to a new survey by Oracle.

The New Digital Demand in Retail Banking, Oracle Financial Services Global Retail Banking Survey 2018

The Oracle research, published on April 11, found that out of the 5,200 customers from 13 different countries polled, 67% have already made the switch to digital, accessing their bank accounts through digital channels and platforms including mobile banking apps and web-based banking platforms.

According to Sonny Singh, senior vice president and general manager of Oracle’s financial services global business unit, consumers are increasingly opting for digital banking for its ease and convenience.

“While customers are generally satisfied with basic banking services, their satisfaction drops when attempting more complex transactions such as securing a loan,” Singh said.

“Banks today must provide a more seamless customer experience or run the risk of losing out to non-banking alternatives.”

Going further, the research also found that as much as 69% of consumers want their entire financial lifecycle on digital channels, highlighting a substantial shift in consumer needs.

The Rise of Challenger Banks and Fintechs

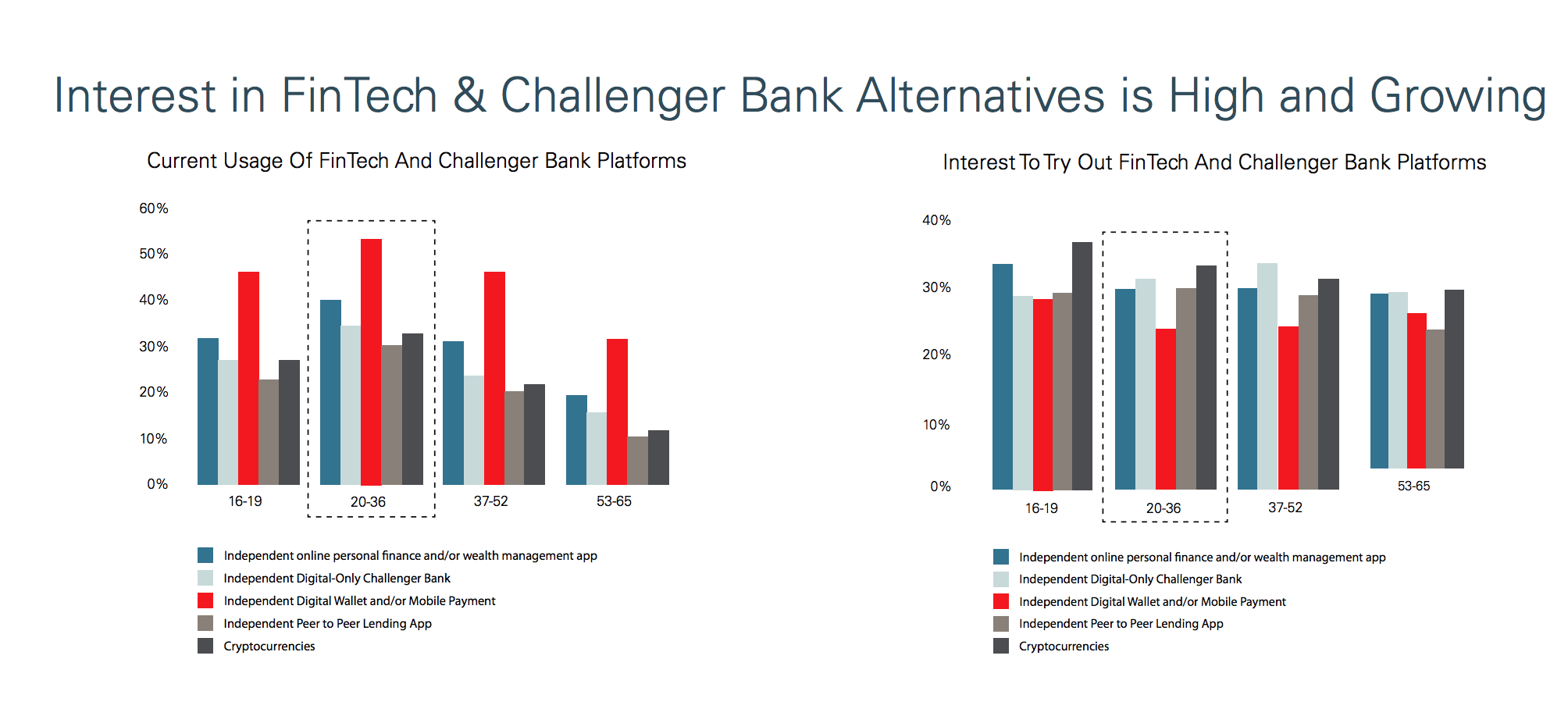

As the top three most important factors for choosing a banking services provides, respondents cited trust, costs and experience. However, when customers go into the banking lifecycle, the costs and experience triumphs trust, making non-bank options an attractive alternative to incumbent banks.

One-third of respondents said they were looking for alternatives for personal loans and mortgages because of the unsatisfactory experience. Other areas that are often unsatisfactory in terms of experience include personal finance and investment.

With the major shifts happening across the consumer financial lifecycle, consumers are showing high interest in exploring challenger bank options at every stage. This high level of interest in alternatives highlights a need for today’s banks to improve services at every financial lifecycle stage, the report says.

More than 40% of customers believe non-banks assist them best in their personal finance management and investment needs.

The New Digital Demand in Retail Banking, Oracle Financial Services Global Retail Banking Survey 2018

“For a long time, financial services have been about buying a product, with little or no service. With powerful technology companies like Google, Apple and Amazon influencing other parts of consumers’ lives, they now are demanding similar levels of personalized digital interactions from their financial services,” said Charlotte Petris, co-founder and CEO of peer-to-peer marketplace Timelio.

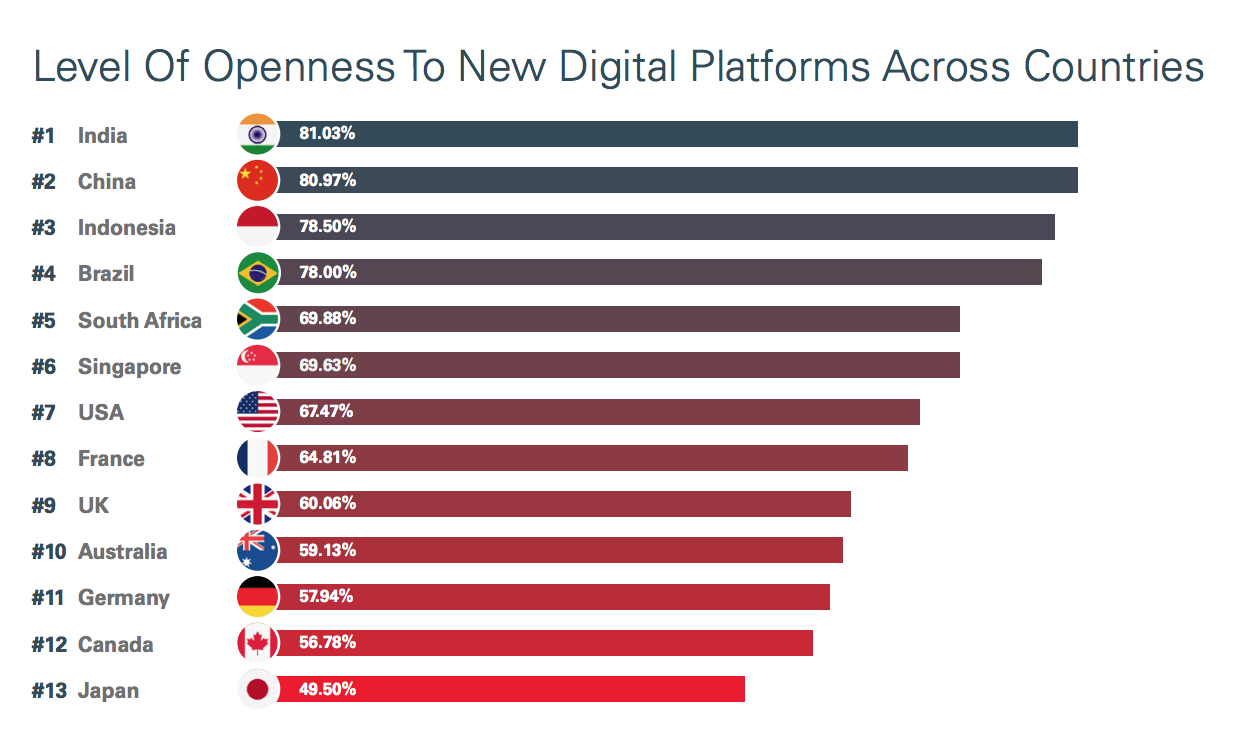

In particular, consumers in emerging economies such as India, China, Indonesia and Brazil, ranked as the most open to trying new digital platforms, while the US fell in middle of the pack at seventh and the UK at ninth.

The New Digital Demand in Retail Banking, Oracle Financial Services Global Retail Banking Survey 2018

“Today, the fastest growing financial services organizations in the world are, without exception, technology-based providers, not incumbent banks or institutions. From Ant Financial, Alipay and WeChat in China, M-Pesa in Kenya, Paytm in India, Kakao in Korea, and more,” said Brett King, founder and chairman of mobile money platform Moven and the author of Bank 4.0.

“Technology allows much faster scale on much thinner margins, but it is fundamentally about a key element in the future of customer-centric banking – the removal of friction.”

Bruno Diniz, a fintech advisor, speaker and managing partner of Spiralem, Innovation Consulting in Brazil, cited the case of Brazil where several fintech companies have become very successful by focusing on specific issues to serve the unbanked.

“The fintechs that are appearing in the Brazilian scene generally offer solutions that are niched and focused in a very specific problem, usually delivering a better experience than the bank offers. The clients are usually underserved by their existing banking provider opening space for them to test fintech alternatives,” said Diniz.

“After some time, the fintech alternatives often set the benchmark for a determined solution such as Guiabolso did with Personal Financial Management and Nubank with credit card segment.”

Mark Smedley, Vice President for Oracle’s Global Financial Services Industry Cloud Solutions, noted that;

Mark Smedley, Vice President for Oracle’s Global Financial Services Industry Cloud Solutions, noted that;

“While GAFA (Google, Amazon, Facebook and Apple) and BAT (Baidu, Ali and Tencent) have become tech, distribution and media platforms of choice for many, Oracle offers an Open Banking Cloud Platform designed to enable Banks and Financial Services institutions to monetize their innovations, innovate with the FinTech and to pursue their own Cloud Platform Strategies. Oracle’s success is defined by how we enable our Financial Services customers to build new digital businesses, products and channels in a collaborative ecosystem.”

The report concludes:

“The future of banking is clear. Today’s banking customers have come to expect the omnichannel experience—service where and when they want it no matter what the platform is. The winners and losers will come down to those who embrace and accelerate change to serve their customers.”