Power has shifted from companies to customers. Mobile phones have become central to our lives. Trust in institutions and traditional advertising has diminished.

New entrants with radically different businesses are capturing our attention, and are reshaping the customer value chain.

These challenges are well documented across business media, research reports and conference presentations. But how should you use this information to understand not only where your customers are today but where they’ll be tomorrow? How can you rethink the basis of competition and pivot your business and operating models to win in the battle for growth?

Traditional demographics, disrupted

For many years now, companies have used demographic data like a customer’s age as a proxy to determine their spending power, likely needs, and relative attractiveness as customers. But these categories do not paint a complete picture. Today, life stages are extended, life events have drifted, and new life stages have emerged – meaning generations are not as predictable or well defined as they once were.

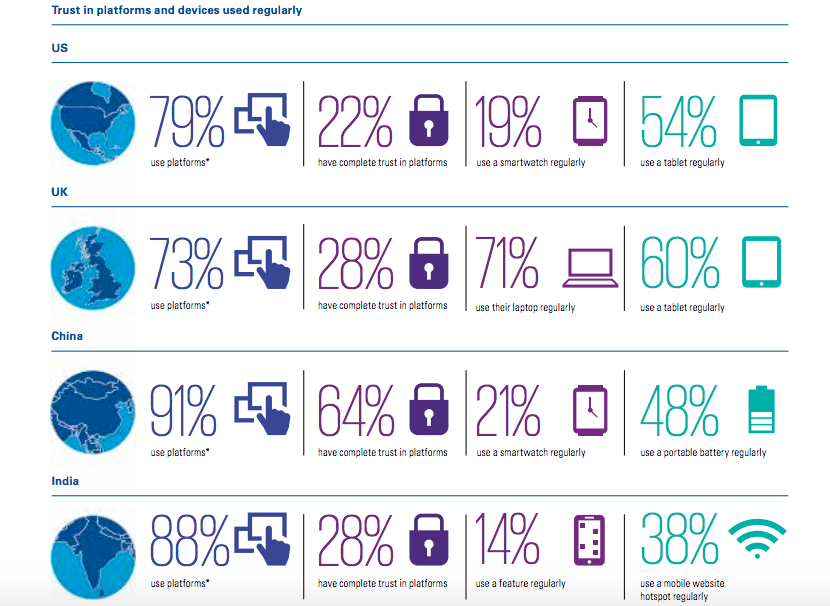

While certain life stages may be enduring, the way different generations approach and move through them is showing signs of change. As our survey across China, India, the UK and the United States revealed, more than two-thirds of millennial respondents had yet to purchase their first home. As a consequence, companies’ assumptions about this generation may be off by several years.

Meanwhile, new stages are emerging. Baby boomers are redefining their next life stage relative to their predecessors. Many are facing unfunded retirement, increased life expectancy, rising healthcare costs and the potential need to provide extended financial support for their millennial children and possibly their parents as well. As a result, what should have been their peak spending years have been disrupted, leaving them facing a new set of challenges. This phenomenon is creating a new life stage for many we call “unretirement” and it is especially pertinent to the banking industry.

We’re witnessing consumers once assumed to be retiring and entering the deaccumulation phase of their lives prolonging (or attempting to) their working lives, sometimes having to compete with more contemporary skills, reinvent themselves with second careers, or take part-time jobs to make ends meet. In addition, working longer is not necessarily perceived to be a bad thing — some people are staying in the workforce longer because they want to.

In our global survey, respondents often replied that they didn’t want to retire. They worry that retirement connotes boredom. They preferred to be active and working as long as they possibly could. However, preferably working on something enjoyable rather than out of necessity alone. As a result, many people aren’t necessarily looking to retire in the same way as the past, and unretirement could play out in unexpected ways.

Another misconception about generational behavior is that it’s clearly defined and delineated by the respective age group. We are seeing behavior transfers between parents and their children happening more rapidly than in the past, much like parents taught and influenced their children, children are teaching and influencing their parents. Technological improvements and economic realities increasingly intertwine generations and, as a result, are accelerating the rate of technology adoption.

Understanding the Echo Effect

This phenomenon, which we call the echo effect, is occurring between baby boomers and their millennial children, as well as between Gen X — ranging from their 40s to mid-50s — and Gen Z — in their teens. The results have unique nuances, which are playing out in unexpected ways. While Millennials and Gen Z are frequently the generations referenced when it comes to digital savvy and high expectations of technology , they have rapidly transferred their behaviors around technology to their Boomer and Gen X parents.

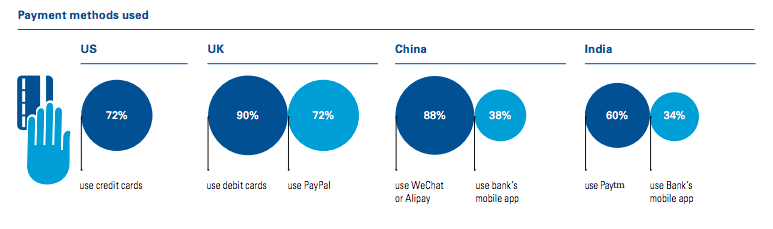

When it comes to the echo effect around financial services, parents serve as a primary influencer and sounding board for advice around money matters while their children heighten their awareness of emerging apps around payments, banking, insurance and wealth management. Many Boomers have been introduced to payment apps like Venmo by their Millennial kids. And our best experiences have become our expectations. When even Boomers have come to expect a seamless experience around making a payment, ordering a car, or buying just about anything on demand, how does your financial services app measure up?

Financial institutions need to be prepared for this new world of changing expectations. Instead of making assumptions about a customer segment based on life stages in the past, banks need to embrace a multidimensional approach to engage equally multidimensional consumers.

A multidimensional approach

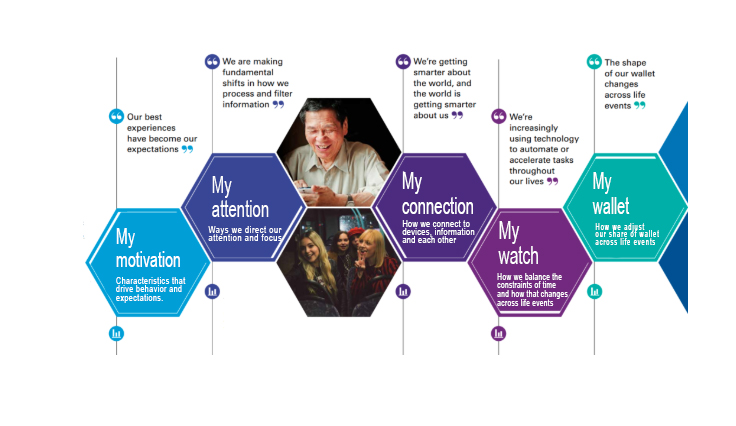

As consumers, our choices have always been influenced and governed by multiple factors, but never has this been as complex and subject to disruption as it is today. This was our impetus to develop the Five Mys framework, designed to help identify what consumers value in an experience, understand the moments that matter to them, get smarter about the connections that contextualize their lives, and learn about the trade-offs they make around time and money.

Many organizations will already explore elements of the Five Mys in isolation, or solely in the context of their category or a specific life stage of their consumer. We believe it is the combination of the Five Mys that generates richer stories, analysis and insight into consumers’ unmet needs, the trade-offs they are making, and the totality of factors influencing their decisions across all aspects of their lives that is simply not possible within a single ‘my’.

The Five My’s Framework

Image Credit: KPMG

How these factors work in concert across the different life stages and life events of a consumer is the key to unlocking real insights, and understanding not just the consumer of today, but predicting what will drive the consumer of tomorrow. This analysis addressing key areas with real business implications, such as:

- the totality of our customers’ wallets, not just income and spending patterns but also wealth accumulation (or net deficits)

- the interrelationship between consumption today and planning for tomorrow, and how this changes the shape and size of the customer wallet — including what’s left in the wallet

- how consumption patterns change across these life stages, and what are the new unmet needs

- the interdependence between generations, and how the financial position of one cohort impacts another, from extending financial support across generations to diminishing wealth transfer as life spans extend and rising healthcare costs erode assets

- the opportunity to play an active part in helping our customers to better plan and prepare for their futures through goal-based planning and the choices they make today.

Understanding the complex underlying drivers of human decision-making has become exponentially more important as the disruption of the digital age accelerates. In this environment, as my colleague Jan Reinmüller has written about recently, customer-first thinking is vital for banks to innovate effectively.

Leveraging the Five Mys framework can help identify the real drivers of customer behavior, leading to more targeted and contextualized experiences, products, and services that create value for both you and your customers.

To learn more about the Five Mys and how to connect with your present and future customers, visit www.kpmg.com/knowyourcustomer