Singapore FinTech Speech by Tharman Shanmugaratnam about Singapore FinTech Festival

by Fintech News Singapore April 19, 2016At the launch of Singapore FinTech Festival at Asia Society, New York, on April 12th, Tharman Shanmugaratnam – Deputy Prime Minister and Coordinating Minister for Economic & Social Policies, also Chairman of the Monetary Authority of Singapore – made a speech on how ranking in FinTech is unncessary, about FinTech tensions and the current and future comprehensive promotion plan for Singapore FinTech.

“I’d like to thank the Asia Society for hosting us this evening, for the launch of the Singapore FinTech Festival. The Festival will take place over 5 days in November this year in Singapore, bringing together technology players, financial institutions, FinTech players and regulators.

We are launching the festival in New York City, and that is not as surprising as it may first seem. It says something about how we view innovation in finance. It is an inherently open system. Innovation is about ideas and enterprise flowing between cities, and connections between players everywhere. We can’t predict how those connections will unfold, but we know that there’s no neat geography that will define financial innovation.”

Ranking in FinTech shouldn’t be focused

To highlight that FinTech is still positioning at a very early stage and that ranking should take neither public- or stakeholders- focus, the speech sent out 2 reasons, including: Singapore’s as well as the FinTech world’s aim of tailoring the transforming finance towards stakeholders’ needs and expectations; and FinTech is expected the world to collaborate and tie up for its development.

“It’s also why we shouldn’t focus too much on the rankings of different financial centres at this stage of the game. You know what they say about the rankings of colleges and universities. If you rank very well, the rank is extremely important. And if you are not ranked well, they are unimportant, irrelevant, and they don’t get to the heart of what you are really trying to do.

Well, we are nicely on both sides of that. Singapore does rank well in the FinTech stakes, but I have to tell you that it’s a distraction at this stage and it really doesn’t get to the heart of what we are doing.

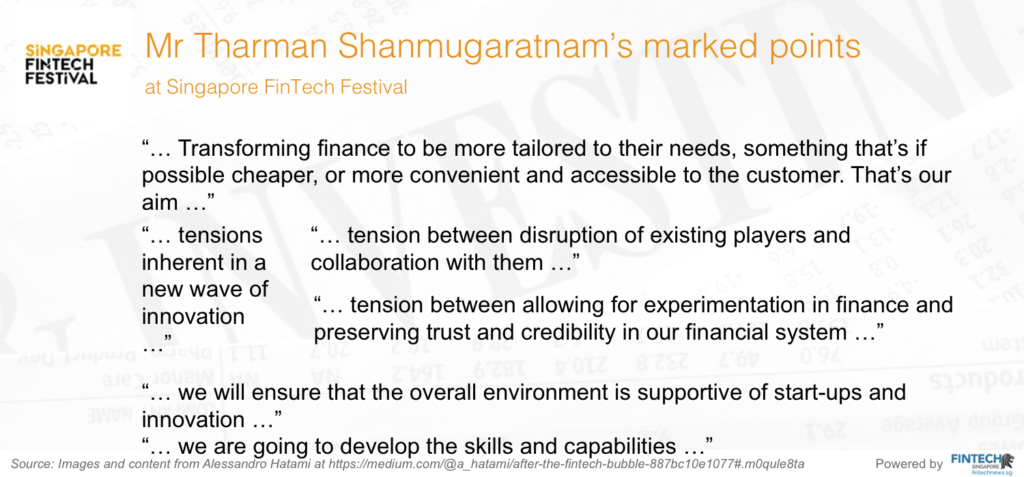

Our aim is not to see if we can be above other financial centres, but to push the envelope and transform finance: to encourage players to find new ways of doing the business, and in a way that makes more sense to the customer – the borrower, the lender, the middle-class investor, or someone who makes payments or receives them. Transforming finance to be more tailored to their needs, something that’s if possible cheaper, or more convenient and accessible to the customer. That’s our aim.

But we are at an early stage in FinTech. We are at the cusp of the new wave of innovation. There’s no assurance that it will succeed, and no telling who will succeed. But it shows much promise – promise of delivering better value to the customer.

There’s a second reason why the rankings are really not the end game, and that’s because FinTech probably more so than conventional finance is going to involve tie-ups and collaborations – between players and between cities, at the same time that it’s an extremely competitive business.

The Asia-Pacific has tremendous untapped potential in finance. There is a very significant underserved market in the Asia Pacific, in Southeast Asia, in China, in India. A very large base of the pyramid, so to speak, that’s not well served by the financial sector in Asia. So there’s tremendous scope for innovation in finance as a way of reaching out to far more people and meeting their needs.

And there’s a new generation of tech-savvy individuals in Asia like elsewhere. They are also averse to paying fees. They too are a prime market for FinTech in Asia.”

Singapore FinTech – the Comprehensive Promotion Plan

The Singaporean comprehensive promotion plan of FinTech covers technology over the different aspects of finance businesses at the vertical perspectives and enhances the power of FinTech infrastructure related to speed, API openness and so on at the horizontal perspectives.

“We are promoting innovation in finance in a comprehensive way in Singapore. It requires a whole ecosystem. It requires bringing a whole range of players together – the technology players, finance players, start-ups, and both global and local Singapore players.

We are also looking at every segment of the financial business. There is scope for innovation across the business – in credit, savings, investing, payments and so on.

But importantly too, we intend to be right there at the frontier with regard to the common technology platforms, or the utilities that can be a very important enabler for innovation in finance – the common platforms that help individual players, produce network effects as more players come on board, and help the market work better.

We are looking at each of the industry verticals to see what common platforms might be needed. Ravi will talk more about this. In trade finance, for example, where we are making good progress.

There are also the horizontal infrastructures that can underpin innovation in a range of industry verticals. Such as the infrastructure for centralized addressing for real time mobile payments. And the efficient and secure storage of data in the cloud. And critically – no one has done this very well in in an organized way, having open APIs, whether private or public APIs in each of our established players. Open APIs can spur innovation in banking and finance.”

FinTech Tensions defined and Singapore FinTech attitudes

2 main tensions, spoken in the speech about FinTech, includes: FinTech disruptions and collaboration; between to allow for experimentation in finance and to preserve trust and credibility in our financial system. To face and tackle these 2 tensions, Singapore government and legislation system set up an attitude of allowing innovation, accepting experimentation and managing by carefully observing the corporate FinTechs.

“There will be tensions as we go forward with FinTech, tensions inherent in a new wave of innovation, that we must accept and manage.

First, the tension between new players and established players, or the tension between disruption of existing players and collaboration with them. Many FinTech players see themselves as disrupters. But there’s also a fair bit of collaboration that’s taking place.

Established financial institutions have been partnering or acquiring new, smaller players with new technologies. Acquiring them either as a defensive mechanism or as a way of bringing disruptive technologies within their own organisation with the hope of strengthening what they offer customers.

It’s hard to say how this will play out in the years to come – hard to say whether the disrupters will indeed disrupt the existing financial business in a significant way. I think it’s too early to say.

In China, we have some major FinTech players, they are no longer new now, those like Alibaba and Tencent. They have become established names. Elsewhere it hasn’t made too much of a difference yet. It is early days.

It’s entirely possible that some new FinTech players will eventually make their mark as enduring brands in finance. But we are also likely to see the growing collaboration I have talked about, between established players and start-ups. It is not a zero sum game. And FinTech ventures are also acting as a catalyst for existing players to reengineer legacy systems.

But most importantly, FinTech is promoting a shift from the traditional focus on products to a focus on customers. It’s about understanding their needs, and finding a way of delivering cheaper, or more convenient and more tailored services to the customer.

The second tension is also important, and which we must be willing to manage. It’s the tension between allowing for experimentation in finance and preserving trust and credibility in our financial system. They are both important and we must be willing to manage the tension.

There was I think, in the first wave of FinTech, a certain breathlessness in the way which new businesses were coming up, and in the way which they were perceived and talked about. Such as, in the (Peer-to-Peer) P2P lending platforms, where the name of the game was often to lend as quickly as you can, leveraging on investments in these FinTech companies.

The scene is now maturing. Some of these new lending platforms in the US and elsewhere are now more concerned with the quality of loans they make. Like banks, whose business is credit underwriting, they have to be good at both data analytics and judgment.

Most FinTech ventures, globally, have indeed not succeeded to date. The real stress test of any new idea in finance is the economic and credit cycle. But even where new players fail, they usually leave behind an idea – an idea to be modified, taken over or improved.

We must allow for this experimentation, but we must do it in a way that preserves trust and credibility in our financial system. That is foremost in our minds.

So regulators are watching this carefully. We have to allow for innovation. But any player that acquires a meaningful scale in finance should expect to be regulated like any other financial institution in their business. There must be a level playing field, and there are to begin with good reasons for why regulations exist.

We cannot stifle innovation. We must let people come up with new ideas, and let them run with it. But once they acquire meaningful scale in the financial sector, they should expect regulation.”

Conclusions: Singapore FinTech today and futures

“Ten years from now, finance will be very different. We can’t say exactly how. But we in Singapore intend to be a key player in innovation in finance. A key player in advancing ways to help consumers with their needs as lenders, borrowers, as makers of payments. In Singapore and the Asia-Pacific. We will go about this very energetically in Singapore, especially in developing common infrastructure or utilities, as I just mentioned.

Ravi will be going through some of our strategies. We are going to put grants to work – grants for any financial innovation in Singapore – on a competitive basis.

Very importantly, we are going to develop the skills and capabilities required to make this a new wave, not just a passing trend. It requires many new skills, as well as some of the old instincts that help ensure sustainability across the cycles. And which preserve trust in finance.

We have a major national program in Singapore called SkillsFuture which we are putting a lot of effort into. Finance will be an important vertical in SkillsFuture: investing in the skills of the future.

Finally, we will ensure that the overall environment is supportive of start-ups and innovation. Not many of the new players will succeed, not many will last. But they will always leave an idea behind, to be modified, taken over or improved.

Thank you very much.”

Source: Content and images from Monetary Authority of Singapore at http://www.mas.gov.sg/News-and-Publications/Speeches-and-Monetary-Policy-Statements/Speeches/2016/Speech-at-the-Launch-of-the-Singapore-FinTech-Festival.aspx