2022 saw the start of a significant consolidation phase for the fintech sector, a trend which is set to accelerate this year as the economic climate continues to deteriorate in the face of elevated inflation, higher interest rates and reduced investment, a new analysis by fintech research company Whitesight says.

In its annual Fintech M&A Roundup, Whitesight looks at mergers and acquisitions (M&A) activity in 2022, providing a summary of notable deals across key fintech segments and revealing consolidation trends that emerged in 2022.

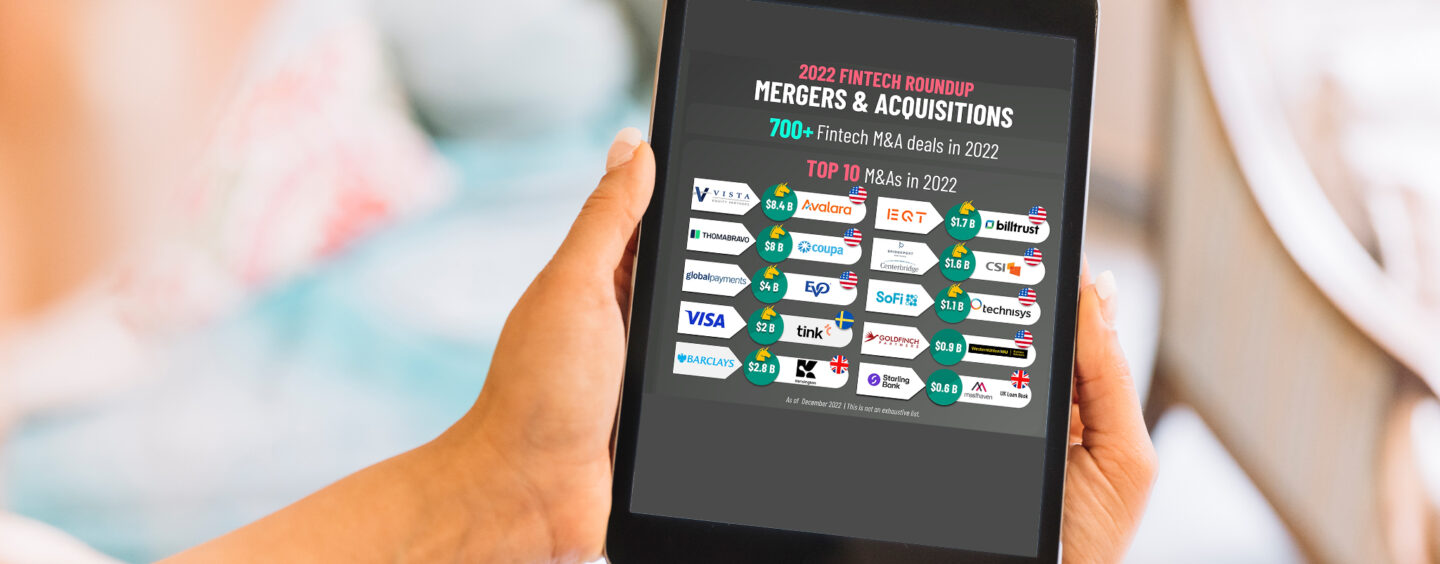

According to the report, 2022 was a year of notable M&A activity for the global fintech sector, which recorded more than 700 deals, among which at least eight billion-dollar transactions.

Top 10 Fintech M&A Transactions in 2022, Source: Whitesight, Jan 2023

These transactions involved both large firms and midsize companies looking to tap economies of scale, expand their scope and gain access to additional tech capabilities, the analysis found.

Companies like Equitable Bank, Razorpay, Bakkt, Sage, Chetwood and ShopBack pursued acquisition strategies to help them expand overseas, increase their market share, enlarge their product offering and tap new business opportunities.

Equitable Bank, a Canadian challenger bank, acquired rival Concentra Bank in February to enhance its scale, capabilities, talent and technology; digital asset company Bakkt brought APEX Crypto, a turnkey platform for integrated crypto trading, in November to bolster its cryptocurrency product offering and expand its footprint into additional client verticals including fintechs, trading app platforms, and neobanks; and Razorpay, a leading payments company from India, acquired Malaysian fintech startup Curlec in February to enter the Southeast Asian market.

These acquisitions came on the back of a challenging macroeconomic environment that triggered a global venture capital (VC) funding pullback and forced investors to decrease their investment pace significantly amid slumping public markets.

The need for financial stability prompted many smaller and less established companies to scamper to merge with other firms to gain access to additional capital and other resources to stay afloat.

Fintech consolidation in 2022 was also driven by efforts from incumbents to access new technologies and remain competitive in the fast-evolving financial landscape. These acquired innovative fintech startups for their tech capabilities, business expertise as well as to access new customer segments.

Financial institutions including Visa, Barclays, JP Morgan and Goldman Sachs got involved in M&A to propel their strategies for open banking, mortgage lending, digital banking, digital payments, and wealth management.

Visa completed in March its US$2 billion acquisition of open banking startup Tink in the year’s fourth largest M&A deal; JP Morgan bought cloud-native paytech firm Renovite in September to modernize its payments infrastructure and enhance its merchant acquiring capabilities; and Goldman Sachs completed its acquisition of NextCapital Group in April, a move that sought to help the bank accelerate the expansion of its services to the growing defined contribution (DC) retirement market through personalized managed accounts and digital advice.

Digital banking, digital payments and fintech infrastructure lead M&A activity

Across all fintech segments, consolidation was most noticeable in three categories, namely digital banking, digital payments and fintech infrastructure, the analysis found.

In digital banking, M&A activity was mainly driven by challengers seeking to acquire competitors in local and foreign markets to expand their footprint and market share, but also to access new products and services such as lending and business solutions.

In Denmark, mobile-based digital bank Lunar made several acquisitions in 2022, snatching up Norwegian digital bank Instabank in March and Danish full-stack payment platform Paylike in July.

In France, Qonto, a digital financial management provider serving small and medium-sized enterprises (SMEs) and freelancers, acquired German competitor Penta in July to drive its expansion to the European country.

And in South Africa, digital bank TymeBank finalized its acquisition of Retail Capital in December, a move that sought to strengthen its business banking offering with SME lending.

Like in digital banking, M&A deals in digital payments focused mainly on expanding product portfolios and gaining access to new tech capabilities such as online payments, account-to-account (A2A) payments, buy now, pay later (BNPL) and rewards.

Such deals included the acquisition of Qfix, a provider of integrated online payments and billing services, by Indian paytech firm Pine Labs; the acquisition of Orchestrate, a provider of fintech infrastructure, by banking-as-a-service (BaaS) company Bloc; and the acquisition of MyCash, a consumer remittance business, by Singaporean neobank INFT.

In fintech infrastructure, segments including open banking, BaaS, core banking, green fintech and environmental, social and governance (ESG) tech, and wealthtech, witnessed strong interest from tech giants and industry leaders.

This trend is evidenced by transactions such as Visa’s US$2 billion acquisition of open banking platform Tink (the fourth largest of the year); Apple’s acquisition of Credit Kudos, a startup that develops software that uses consumers’ banking data to make more informed credit checks on loan applications; and Nasdaq’s acquisition of Metrio, a software-as-a-service (SaaS) climate tech company.

The fintech industry’s consolidation phase is projected to continue in the coming years, Whitesight predicts. And though this may lead to short-term disruption, it will ultimately result in a strong and more resilient fintech industry that’s better equipped to weather future headwinds, the report says.

Featured image credit: edited from freepik