Open finance, the next step in the open banking movement that broadens the scope to a wider range of products and services, offers new growth and distribution opportunities for banks, fintechs and other financial services providers.

In Southeast Asia, regulators are establishing the foundations for open finance as part of broader national modernization reforms and with hopes that the seamless and secure sharing of customers data will help improve financial inclusion.

In a new report, financial software provider Brankas and Southeast Asia-focused venture capital fund Integra Partners looks at the state of open finance in the region, highlighting the key initiatives launched so far.

The report says that in the region, central banks are eager for open finance. It notes however that the strategy varies from one country to another with some preferring a market-led approach, while others have embraced a regulatory-driven approach.

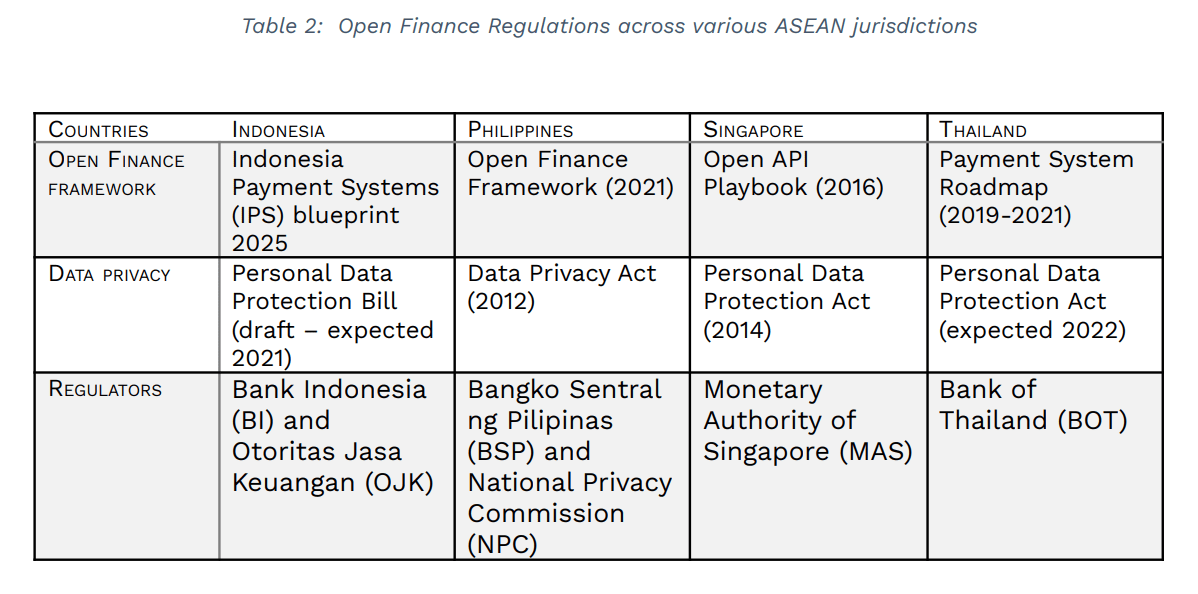

Open Finance Regulations across various ASEAN jurisdictions, Source- White Paper- Embracing Open Finance in Southeast Asia, Brankas and Integras Partners, July 2021

The Philippines

In the Philippines, the Bangko Sentral Pilipinas (BSP) approved new guidelines for the Open Finance Framework in June 2021, allowing for consent-driven data portability, interoperability, and collaborative partnerships among financial institutions and third-party providers.

Under the framework, consumers will have the power to grant financial institutions access to their financial data and will be offered tailored products and services that represent better deals.

An industry-led self-governing body called the Open Finance Oversight Committee (OFOC) will exercise governance on the activities and participants of the Open Finance ecosystem. BSP governor Benjamin E. Diokno said earlier this month that the creation of the committee will be completed within the year.

Indonesia

In Indonesia, regulators have expressed support for open banking as part of the digital financial transformation reform. In 2019, Bank Indonesia put in place its Indonesia Payment System Vision 2025, laying out five main key areas of focus: open banking; retail payment systems; financial market infrastructure; data; and regulatory, licensing and supervision.

Indonesia’s Personal Data Privacy (PDP) bill is expected to pass later this year.

Thailand

In Thailand, although there is no formal guidelines around open finance, the government has been supportive of digital transformation initiatives for the industry notably through the National e-Payment Maser Plan, a scheme focusing on the development and promotion of more effective, safer and lower-cost electronic payment services.

The plan lays out a few initiatives paving the ground for open banking, including the establishment of a working group to test bank statement sharing among financial services companies, as well as the creation of an interoperable infrastructure that would feature, among other things, biometric capabilities for identity authentication and electronic know-your-customer (eKYC).

These efforts sit alongside the implementation of the Personal Data Protection Act (PDPA), a legislation introduced in May 2019. PDPA, which came into full effect in June 2021, mandates that data controllers and processors who use personal data must receive consent from data owners and use it only for expressed purposes.

Singapore and Malaysia

Finally, in Singapore, though there is no mandatory requirement for banks to implement open banking, the Monetary Authority of Singapore (MAS) has supported the trend through notably the launch of the Finance-as-a-Service API Playbook, which contains principles on API governance, implementation, use cases, design principles, and 400 recommended API services.

MAS has also been involved in the launch of the API Exchange (APIX), a global, open-architecture platform that serves as a marketplace for fintech and financial institutions to connect, share ideas and innovate collaboratively.

Similarly to Singapore, Malaysia has taken a market-driven approach to open banking with a non-mandatory guideline framework for working with open data and open APIs.

Vietnam, Cambodia lag behind

Across Southeast Asia, the Philippines, Indonesia, Thailand, Malaysia and Singapore have so far been the most proactive jurisdictions to embrace open banking.

In Vietnam, although banks are becoming increasingly aware of open banking and recognizing the need to embrace open APIs to keep up with the rapidly evolving financial landscape, there’s been no real commitment from the government nor regulators so far on the topic.

Similarly, Cambodia currently has no regulation around open banking and customer data protection.

Untapped opportunities

Southeast Asia’s fast-evolving and yet still largely underdeveloped open finance ecosystem is becoming an appealing market for services providers looking to tap into this region’s large population of unbanked and digital reforms. In June, Singapore-headquartered open finance API platform Finantier raised an undisclosed seven-figure round to expand across the region, citing the region’s huge unmet demand for financial services.

According to Bain, over 70% of adults in Southeast Asia lack access to financial services, and millions of small and medium-sized enterprises (SMEs) in the region face large funding gaps. This is partly because many financial institutions are lacking access to customers’ financial data, limiting thus their ability to assess these customers’ eligibility for products or services.

With open finance and data sharing, banks can partner with third-party providers such as online marketplaces to gain access to alternative data including ecommerce transaction data to assess the credit risk of previously underserved customers.

Open finance also allows banks to lower the cost of customer acquisition and onboarding by allowing them to partner with third parties for eKYC, expanding thus access to underserved customers.

Featured image credit: Technology photo created by rawpixel.com – www.freepik.com