As technological advances significantly change people’s daily lives, the benefits from these advances essentially boil down to one aspect, convenience. Technology has allowed business and social activities to expand and remain primarily online.

This includes transactional decisions from purchasing tangible and non-tangible products, making business decisions and investments to immersing oneself into an augmented reality where connections happen regardless of distance.

But with convenience comes negligence. At the other end of this double-edged sword is the possibility of fraud. Cybercriminals are lurking around every corner to find loopholes in systems as more businesses and consumers shift their behaviors to a more digital approach.

Hackers and fraudsters are no longer limited to well-trained software engineers or computer experts. In today’s world, technological convenience has made it so that an average Joe could be behind a fraud event, which might result in losses worth millions of businesses’ and consumers’ funds.

Digitised Fraud in Numbers

Similar to how consumer fraudsters cheat and scam via phone calls or face-to-face interactions, fraud happens in financial technologies — except at a much faster, breakneck speed than traditional methods.

According to The Asian Banker, the incidents of fraud around the Asia Pacific (APAC) region shot up exponentially during the beginning of the COVID-19 pandemic. Financial institutions were encouraged by central banks to prioritize digital transactions and were incentivized to do so as part of the contactless approach to contain the virus’ spread.

The government-imposed lockdowns, quarantines, and working-from-home arrangements have only accelerated the transition to digitalized transactions. In the first quarter of 2021, fraud incidents more than doubled (178 percent) compared to the last quarter of 2020. Online banking fraud and account takeovers are the top two incident types at 250 percent and 650 percent higher, respectively.

Singapore had more than 15,000 reported scam cases in 2020 alone, a record 65 percent increase from the previous year. This resulted in a loss of SG$32 million, with cyber extortions accounting for SG$790,000.

Across the causeway, there have been multiple reports in Malaysia that funds were transferred without the account holder’s authorisation. According to the country’s Commercial Crimes Investigation Department, from 2020 until May 2022, there was a total of 71,833 reported scam incidents amounting to RM5.2 billion in losses to the victims.

Malaysia’s financial services firms have seen a significant increase in fraud cost of 15.4 percent in three years. Malaysia is also experiencing the highest monthly volume of successful fraud attacks in the region with its financial services seeing a 22 percent growth in volumes in three years.

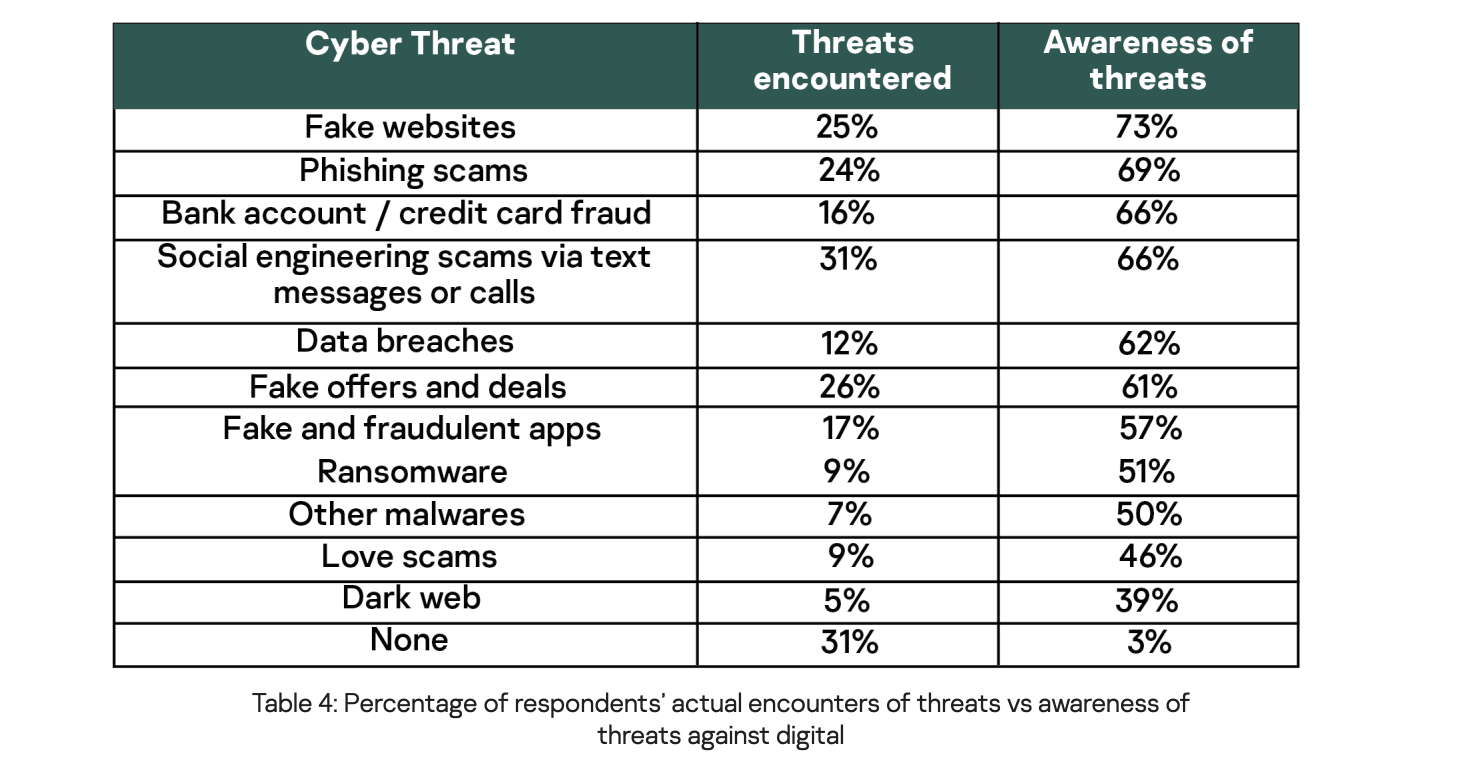

Public awareness of such fraudulent scams is relatively high in APAC, but awareness does not necessarily increase prevention, at least in cases of fintech-related fraud. APAC Corporate Communications at Kaspersky conducted a survey in which an overwhelming 97 percent of respondents in APAC were aware of at least one type of threat against a digital method. In contrast, two-thirds of respondents have encountered at least one type of threat themselves.

Mapping a secure path for the future of digital payments in APAC, Kaspersky

The study highlighted a more in-depth analysis of fraud cases in APAC, with financial losses from cyber threats capped at up to US$5,000, with a smaller percentage reporting a loss of more than US$5,000. But despite the relatively low sum of financial losses, each loss accumulates into significant amounts, and arguably the biggest loss would be the loss of trust from consumers in the fledgling fintech market.

Corporate fintech fraud is on the rise, too, particularly among e-commerce companies. Alternative payment methods such as digital e-wallets and buy-now-pay-later (BNPL) services are the most targeted. According to its Q1 2022 Digital Trust & Safety Index, Sift reported a 200 percent hike in payment fraud in digital wallets and a 54 percent year-over-year increase in BNPL services. Even the supposedly safe haven of crypto exchanges saw a 140 percent increase.

Countermeasures against Fraud in Fintech

Experian’s Global Identity & Fraud Report reported, “Four in five APAC consumers (80 percent) expect businesses to take the necessary steps to protect them online, reflecting global trends where nearly three-quarters of consumers expect businesses to do so.”

The report also added that consumers are starting to view online security as a legitimate trade-off for businesses collecting their data. They expect businesses to protect them from online threats related to their systems or too complex for consumers to handle.

Protection against fintech fraud is now viewed almost as a form of corporate social responsibility amongst digital service providers. The most common suggestion is to add more secured verification, such as 2-Factor authentication (2Fa), or increase the number of verification steps to safeguard clients’ financial assets. But is having more friction to verification the best solution?

Aravind Narayan

According to Sales Strategy & Execution Global Director of C3PRS (Data & Analytics), Aravind Narayan, effective fraud preventions in fintech includes customer onboarding that

“efficiently screens customers against smart screening datasets, verifies customer information against trusted data sources and authenticates customer documents to ensure that they are not fraudulent”, ongoing monitoring, and screening of transactions for any unexpected purchasing behavior or billing.

He added that although strict compliance processes must be implemented, it must not be at the cost of the seamless and customer-friendly experience that separates the fintech industry from its predecessors.

Jane Lee

Jane Lee, Trust & Safety Architect at Sift, wrote that fraud prevention could occur in real-time by utilising automation and machine learning of user behaviors. Once suspicious behavior is detected, the fraud team can “evaluate the risk and decide the types of friction to apply”. Educating consumers is a proactive way to prevent fraud, and businesses must take engaging customers about fraud seriously, according to Lee.

She further warned businesses that consumer loyalty would waver and shift if satisfactory actions are notaken to circumvent fraud on their platforms. According to Sift’s Q3 2021 Digital Trust & Safety Index, around 74 percent of consumers say they would stop engaging with a brand due to fraud.

Extra caution and due diligence

The consumers’ side will have to be extra cautious and do their due diligence about the company or service they are using. Spiceworks’ Business & Finance points out that consumers can use antivirus software to protect themselves. Albeit a license fee and regular updates are needed in between, it is a small cost to bear compared to the potential exorbitant losses resulting from financial fraud.

Another timely reminder is that consumers should avoid sites that are flagged as unsafe. Browsers like Google Chrome and Safari have ramped up their security systems and can detect sites that are deemed suspicious. There will be an alert for the user, warning them of potential dangers visiting the website.

The ever-evolving digital landscape means that eliminating the possibilities of fraud 100 percent is next to impossible. As challenges to keep cybercriminals at bay become more complex, financial service firms must put safety measures in place without compromising growth, and consumers must remain vigilant over their financial assets.