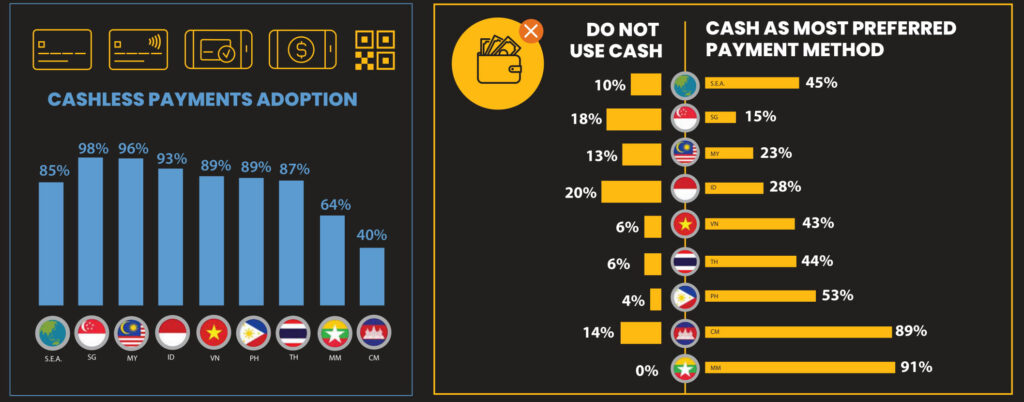

Within Southeast Asia, 85 per cent of consumers adopt some form of cashless payment solution, a study by Visa has revealed.

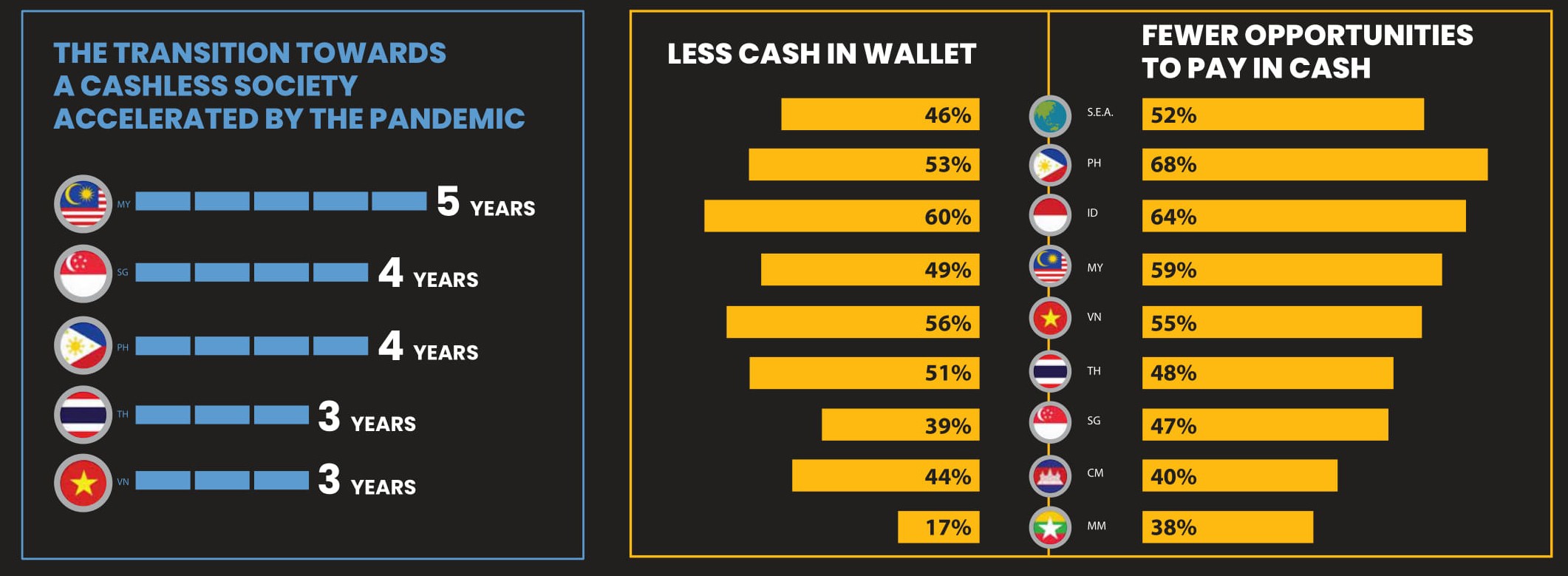

Visa’s Consumer Payment Attitudes Study 2021 also found 46 per cent of Southeast Asian consumers carry less cash in their wallets compared to before the pandemic, particularly those in Indonesia, Vietnam and Thailand.

Visa’s Consumer Payment Attitudes Study 2021

Besides uncovering payment trends across the region, the study delved into the digital banking industry and made several key findings. Among them, 77 per cent of consumers were willing to bank with a well-known brand that is not currently in financial services.

Here are the key narratives published.

Cashless payments gaining traction

While Singapore (98%), Malaysia (96%) and Indonesia (93%) lead the way for the adoption of cashless payments within Southeast Asia, countries such as Vietnam, the Philippines and Thailand are still playing catchup with an average adoption rate of 88 per cent.

Visa’s Consumer Payment Attitudes Study 2021

In contrast, cashless payments remain nascent in Myanmar and Cambodia with only 64 and 40 per cent of consumers utilising them respectively.

The pandemic has played a significant role in accelerating the adoption of cashless payments. The study found transitioning towards a cashless society was accelerated by three to five years across various Southeast Asian countries.

While the increased risk of contact infection associated with cash did drive the adoption of cashless payments, e-commerce’s meteoric rise also played its part.

The pandemic paved the way for new online shopping habits for consumers in the region. Online shopping has boomed particularly in Thailand, with 65 per cent of Thai consumers shopping online for the first time via apps or websites. Over half of consumers in Indonesia and the Philippines also reported being first-time online shoppers.

The growing acceptance by merchants and increased security of cashless payments were other key factors that accelerated the adoption of cashless payments.

Meanwhile, bill payments and supermarket purchases are expected to be the first categories to go fully cashless due to their routine and recurring nature. Online travel is expected to follow with the convenience of making pre-payments online.

Fragmented payments landscape

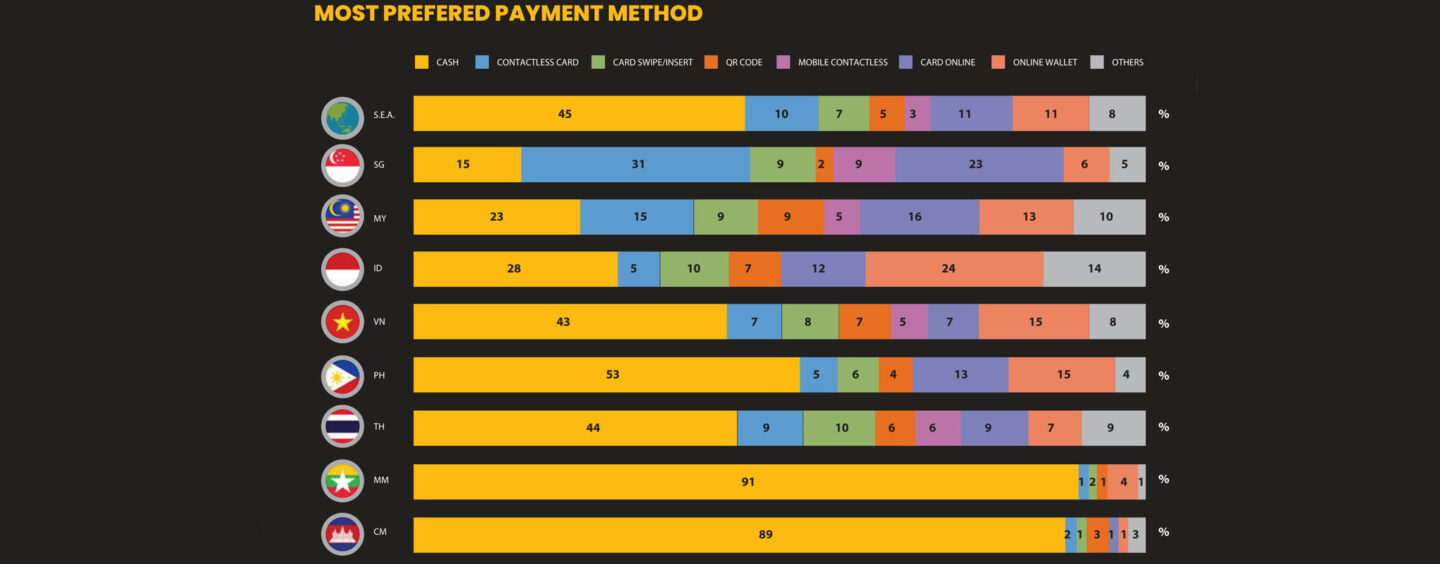

As the number of digital payment methods gains traction across Southeast Asia, consumers now have an abundance of choice. Hence, the payment preferences of consumers are diversifying, creating a fragmented regional payments landscape.

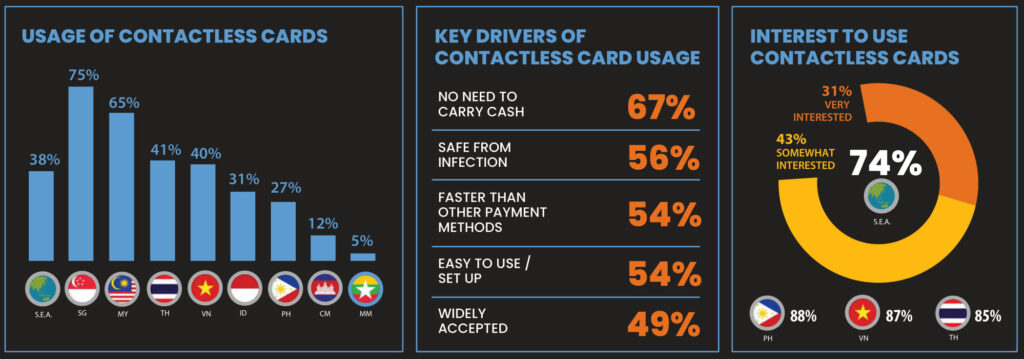

For instance, contactless cards are most preferred in Singapore, likely due to widespread acceptance among merchants. In contrast, online wallets lead the way in Indonesia due to the multitude of e-wallet players such as GoPay and Ovo.

As a region altogether, e-wallets (11%) and contactless cards (10%) were the most preferred digital payment methods.

E-wallets vs cards

While e-wallets are preferred in markets such as Indonesia, Vietnam and Myanmar, cards remain the favoured choice for payments in Singapore and Thailand.

Consumers shared e-wallets were preferred due to the speed of transactions and convenience they offered. Minimising physical contact was another reason cited, given the current circumstances.

Meanwhile, cards were favoured as they were more widely accepted by merchants. However, this narrative is unlikely to continue as more merchants are accepting e-wallets, driven by lower processing fees offered by such platforms.

Visa’s Consumer Payment Attitudes Study 2021

Digital banking rising throughout SEA

Favourable regulatory policies are set to encourage digital challenger banks to enter the regional banking industry.

According to the study, 66 per cent of consumers within Southeast Asia are interested in digital banks. This statistic is highest in countries such as Thailand (83%) and the Philippines (81%).

Surprisingly, consumers in Singapore rank third-lowest, with only 59 per cent interested in digital bank offerings. This could be attributed to the strength of incumbent banks. With Singaporeans generally satisfied with current banking solutions, there is a less urgent need for digital challenger banks.

Convenience was the primary driver for digital banking among consumers – time saved by avoiding physical queues and the ability to bank any time of the day were among the top reasons cited.

Meanwhile, doubts remain over the security of digital banks. Consumers expressed concerns over unauthorised transactions and the risk of hacking. A preference for human interaction represented another challenge for digital banks to overcome.

Types of digital banking providers and services

The majority of consumers in Southeast Asia are interested in digital banking services provided by traditional banks (89%). However, there is an opportunity for challengers to disrupt the region’s banking landscape.

77 per cent of consumers are willing to bank with a well-known brand that is not currently in financial services. This trend has been observed among digital banking players across the region.

In Singapore, Grab-Singtel was awarded a digital banking license while many parties have shown significant interest in Malaysia’s digital banking license.

Consumers have also shown higher interest in digital banking services that are more likely to impact their day-to-day lives.

Services such as peer-to-peer money transfers, bill payments, deposits and withdrawals were preferred. In contrast, investments, international money transfers and loans were less desired.

This could be due to the preference for these high-value transactions to be carried out by a trusted incumbent bank instead of an unproven digital one for a sense of assurance given the increased financial risk.

Featured image: Photo by Ivan Samkov from Pexels