Singapore is Now Considering Virtual Banking Licenses Too—Here’s Why

by Fintech News Singapore May 7, 2019The now famous Hong Kong virtual banking licenses have been a bit of a mixed bag for the region, but nevertheless, it’s gotten a lot of attention. To date, four licensees will be ready to go to market before the year closes.

Singapore has indicated that they want a slice of that action too.

The Monetary Authority of Singapore (MAS) stated that it is studying the licensing regime to see about admitting fintech firms without a traditional bank at its core. The statement from MAS came a day after DBS Bank’s Piyush Gupta said that he sees no reason why the regulator would not in a TV interview with Bloomberg.

The move was probably only a matter of time, as Singapore and Hong Kong have been in a stiff battle for the Asia fintech hub status for many years now, though ostensibly, both are amicable enough to forge strategic partnerships.

Our neighbour from across the causeway, Malaysia, also wants to pave the way for virtual banks, and will release its requirements for a virtual banking license by the end of this year.

Singapore is known to be relatively experimental with its fintech, most recently via a trial with Canada to conduct cross-border payments with a central bank backed digital currency, via Project Jasper and Project Ubin, respectively.

More pertinently, e-wallets have achieved a significant level of ubiquity in Singapore that its populace is at least educated about digital money, whether or not they decide to utilise it. With an interest in fostering the oft-touted cashless society, virtual banking is the next natural step for Singapore.

The Timing Can’t be Better

The banks may be virtual, but the cards are often real and usable (Image credit: N26)

These digital only banks go by many names: virtual banks, neo banks, challenger banks, etc, but mainly they indicate banks that are fully operational online, and often, offer 24/7 service that could be disruptive of incumbent banks that lock you into only utilising them during banking hours.

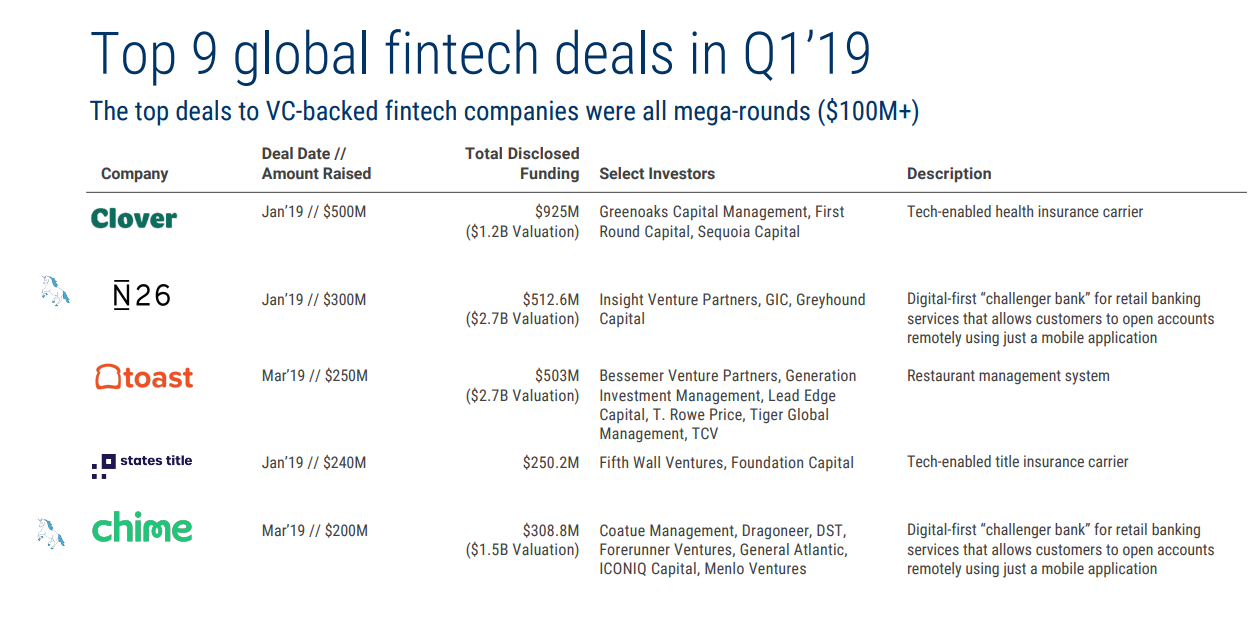

It’s not surprising then that in CB Insights‘ first 2019 report for fintech funding, the company noticed an interesting trend about fintech funding for virtual banking—that it’s on its way towards hitting critical mass.

The figure below, showcasing funding into global virtual banks in recent years paints a picture about virtual banks’ future.

Image Credit: CB Insights

Many of these banks aren’t even three years old, and yet they are able to pull significant numbers due to a variety of factors:

Though educating the general public about virtual banks can be tough, especially if one wants to stand out above the multitudes of online money scams, virtual bank operations can be cheaper than a regular bank. In the best of circumstances one may only need customer service operatives on the phone, and people to deal with the tech and backend.

Having all of your operations online through a web browser or app also allows for more automated processes, and robust data analysis on trends and behaviours. Being online means that virtual banks are able to offer more personalised banking services to crowds that may have been underserved before, and do so profitably.

The selling point is there, all it needed were success stories, and enough time and advocacy for these virtual banks to soar. For all intents and purposes, 2019 seems to be that year for the scene because according to the same CB Insights report, two funding rounds in 2019 propelled two challenger banks into unicorn status.

Image Credit: CB Insights

The unicorns are part of an ongoing funding stream into challenger banks lately, while there was a slowdown following a promising start to 2018, funding activity has ramped up again with the two new unicorns, N26 and Chime.

Image Credit: CB Insights

Investors seem excited to pour money into the next big virtual bank, and MAS seems to want to cash in on this trend. The question is now, will the virtual banking license help cultivate any of its homegrown names, or will an international player swoop in to take it all in Singapore?

Revolut is a UK-based virtual bank, and arguably the reason why virtual banks are so vogue. And it has made a huge stake in Singapore, even set up its Asia Pacific headquarters here. After winning licenses from the regulator, Revolut is also working with MAS to shape the upcoming Payment Services Bill most recently at its second reading.

Even from the ground-up, Singapore is already getting input from an international firm, so there could a cause for concern here.

Execution is Key

Hong Kong’s move to introduce the virtual banking license has been lauded by many and saw huge interest when it was just announced, but criticisms have since emerged about punishing requirements.

David Rosa and Jack Zhang, founders of Neat and Airwallex. (Image Credit: Neat and Airwallex)

Hong Kong-based virtual bank Neat was one of the first to publicly speak out about the virtual banking license by the Hong Kong Monetary Authority (HKMA), preferring to pick up the money lender license instead.

To Neat, the minimum capital requirement of HK$300 million, a requirement for high profile board members, and strict IT security structures would preclude them from offering their existing services to the underserved profitably—which was the company’s entire reason for existing.

In contrast, Neat’s founder David Rosa references UK’s regulations, which only require €5 million in minimum capital for a license to encourage entry of niche players and neo-banks.

Later, a Tencent-backed virtual bank, Airwallex, echoes Neat’s sentiments about the requirements, which they opine could affect their ability to offer new banking products and services.

HKMA seemingly had investors as a priority when drafting its rules, and had the understandable impulse not to rock the boat too much.

An argument could also be made that the restrictive minimum capital requirement was by design, in order to ensure that if Hong Kong’s populace does port over to virtual banking, then the fidelity of the state’s economy can be maintained without too much overhaul in the future.

The Monetary Authority of Singapore now has to undertake the difficult job of walking a thin line with both sides of the virtual banking tightrope.

Given Singapore’s track record, it is likely that Singapore’s own eventual virtual banking will veer closer to the UK’s relatively more lax regulations, rather than Hong Kong’s, though of course, only time can tell.

Featured image via MAS