How Fintech and Digital Platforms are Driving Financial Inclusion Around the World

by Fintech News Singapore January 20, 2022In both advanced and emerging economies, new digital platforms are helping to advance financial inclusion by improving access to payment services, credit, insurance and wealth management.

In a new working paper titled Platform-based business models and financial inclusion, the Bank for International Settlements (BIS) looks at the role of digital platforms in increasing financial inclusion, noting that over the past years, access to financial services has considerably improving, a trend that correlates with the rise of fintech adoption.

Bigtechs drive financial inclusion in China

In China, tech giants including Tencent and Ant Group have played a key role in improving financial inclusion, leveraging their parent companies’ activities and footholds in e-commerce and social media to provide low-cost payments, credit, insurance and savings products to hundreds of millions of users.

Ant Group, which counts 1.3 billion users, owns one of China’s largest digital payment platforms, Alipay, and one of the biggest money-market funds in the world, Tianhong Yu’e Bao. It also runs Zhima Credit, a third-party credit rating system. In 2019, Alipay handled US$17 trillion worth of transactions, which was more than Visa and Mastercard combined.

Tencent, a tech and entertainment firm, operates WeChat, a social application that had some 1.2 billion active users in 2020. Its in-app payment system, called WeChat Pay, has over 900 million users, according to Business of Apps. In the last quarter of 2019, WeChat Pay managed over one billion business transactions of online payment per day, data from Statista show.

Public digital infrastructures fuels finance innovation

In India, the rise of digital platforms has been propelled by the introduction of public infrastructures including the digital identity system Aadhaar, and real-time payment infrastructure the Unified Payment Interface (UPI).

These systems are part of the so-called India Stack, a project that’s been in the works for a decade now, and which seeks to create a unified digital infrastructure to bring the population into the digital age.

The India Stack comprises four layers of infrastructure and standards: digital identity, an interoperable payment interface, digitalization of documentation and verification, and a consent layer.

At the same time, India has seen the emergence of a burgeoning fintech ecosystem that today counts 2,100 companies, among which 17 unicorns worth US$1 billion and over, data from Invest India, the national investment promotion and facilitation agency, show. These figures make India the third largest fintech ecosystem globally.

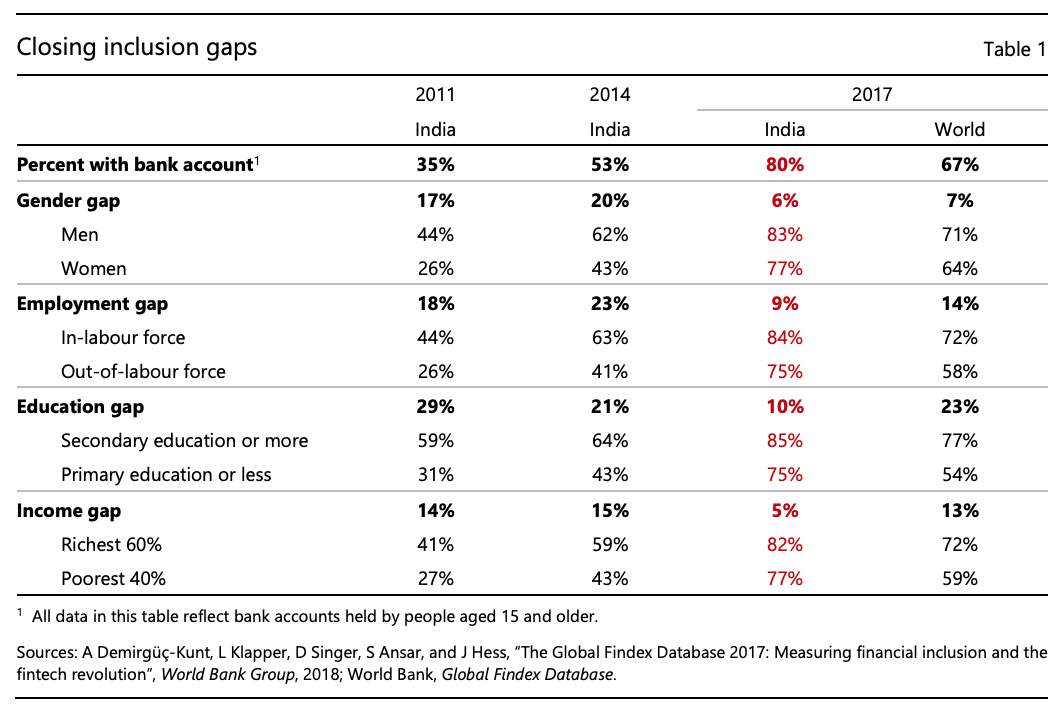

Overall the combination of public infrastructures, government-led financial inclusion initiatives and privately operated platforms has helped India to drastically increase access to financial services. Between 2011 and 2017, some 470 million Indian adults opened a bank account in a financial institution. The share of the population with bank accounts soared to 80%, up 45% points from 2011 at 35%, data from BIS show.

Financial inclusion in India, Source: Bank for International Settlements (BIS), The design of digital financial infrastructure: lessons from India, 2019

Africa: a leader in mobile money

In sub-Saharan Africa, the rise of mobile money platforms has been a catalyst for the financial inclusion of millions of those previously underserved by the traditional banking sector.

In 2020, 1.21 billion mobile accounts were registered globally, with 548 million of those accounts being located in Africa. The figure makes Africa the world leader in mobile money adoption, data from mobile industry organization the GSM Association (GSMA) show.

In the region, the launch and growth of mobile money and other digital financial services has considerably helped improve financial inclusion.

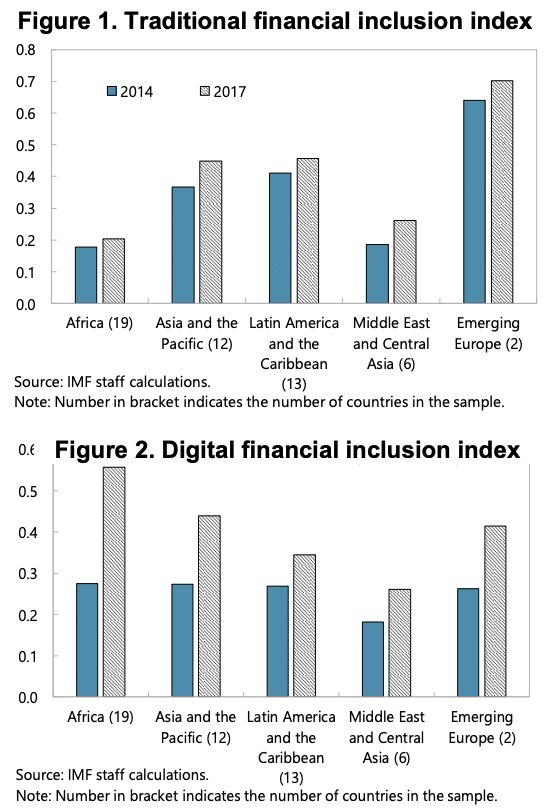

Research by the International Monetary Fund (IMF) found that although traditional financial inclusion has increased meagerly between 2014 and 2017, digital financial inclusion on the other hand soared in the same period, helping propel access to financial services.

Financial inclusion indexes, Source: International Monetary Fund, Is Digital Financial Inclusion Unlocking Growth? 2021

Improving financial inclusion in advanced economies

Besides emerging markets, digital platforms have also had a positive impact on financial inclusion in advanced economies.

In the UK, the government started implementing open banking in 2017 as the local equivalent to the Second Payment Services Directive (PSD2) in the European Union (EU).

Aimed at stimulating increased competition and innovation in the financial services industry, open banking mandates the UK’s nine biggest to release their data in a secure and standardized form so that it can be shared easily between authorized organizations.

As of January 2022, 4.5 million customers were regular users of open banking, among which 3.9 million consumers and 600,000 small businesses, according to the UK’s Open Banking Implementation Entity (OBIE).

Besides open banking, the UK’s fintech ecosystem has generated a number of platform-based offerings and digital solutions designed to broaden access to financial services.

ProxyAddress, for example, provides duplicate, or proxy, address details to those facing homelessness. In October 2020, the startup launched a pilot in London to offer Monese accounts to those without stable address details.

The UK’s Financial Conduct Authority (FCA) estimates that between 2014 and 2020, the banking sector successfully reduced the number of adults believed to be unbanked from 1.71 million to 1.2 million.