Mastercard’s Study Shows That Buy Now, Pay Later Is Rising in Popularity in APAC

by Fintech News Singapore November 10, 2022Buy now, pay later (BNPL) options are rising in popularity in Asia-Pacific (APAC) where consumers are increasingly turning to these payment arrangements to pay for bigger-ticket items like electronics and appliances, findings from a Mastercard study show.

A survey conducted by Mastercard World Payments Advisory of 50,000 consumers in over 50 markets, found that interest in BNPL in APAC has risen over the past year.

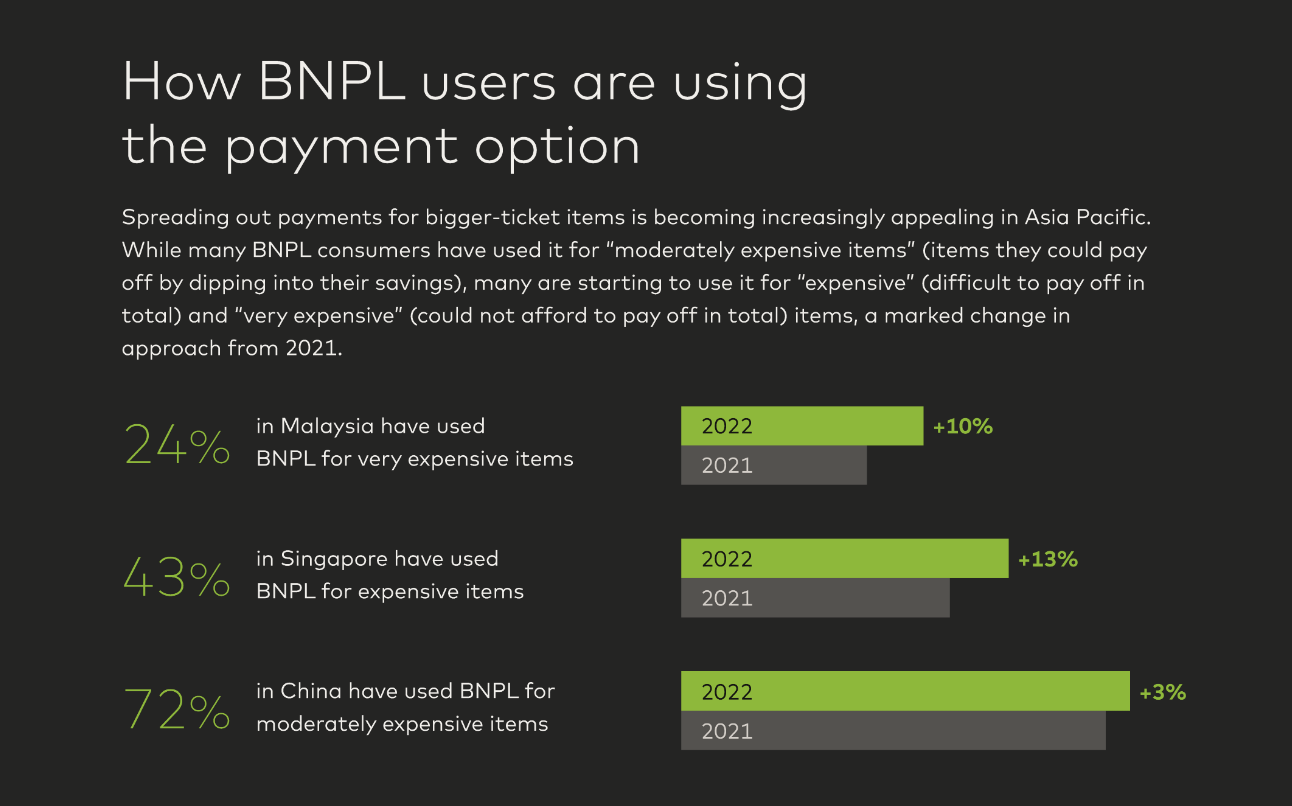

In China, 72% of BNPL users surveyed said they have used the payment option for very expensive items, up 3 percentage points from 2021. In Singapore and Malaysia, that proportion stands at 43% and 24%, representing a 13 and 10 percentage point increases from last year, respectively.

How APAC BNPL users are using the payment option, Source: Mastercard World Payments Advisory, 2022

Preferences differ from one country to another, but overall, consumers shared high interest in using BNPL arrangements at locations where they are most likely to make a purchase. For consumers in India and South Korea, that location is clothing and apparel stores where 38% and 22% of respondents, respectively, indicated being interested in using BNPL.

In China and Thailand, it’s wholesalers and hypermarkets. In each of the two locations, 33% of respondents said they are interested in using BNPL.

And in Vietnam and Malaysia, 49% and 29% of respondents, respectively, showed interest in using BNPL for electronics and appliances.

Where APAC consumers are using BNPL, Source: Mastercard World Payments Advisory, 2022

BNPL, a type of short-term financing that allows consumers to take purchases and pay for them in installments, often interest-free, is a booming market in Southeast Asia. A Google, Temasek and Bain report released last year forecasted the digital lending industry, which includes BNPL, to hit US$92 billion in transactions in 2025 in the region, up from US$23 billion in 2020.

In the region, the market is dominated by specialized fintech startups such as Kredivo, Atome, and Akulaku, which use advanced technology and leverage investment support to aggressively expand their footprint, broaden their customer base and continuously enhance their BNPL capabilities.

Kredivo has more than four million users in Indonesia, representing over 50% of the local BNPL market; Atome, which is part of Advance Intelligence Group, currently partners with over 15,000 online and offline retailers in ten different markets; and Akulaku claims 26 million users across Indonesia, the Philippines and Malaysia.

But across the region, other players are also entering the space, making the sector increasingly competition. Established e-commerce platforms like Shopee and Lazada, ride-hailing platforms such as Grab and GoJek, and tech firms like Sea, are all offering their customers short-term loans to help them pay for a variety of products and services, including taxis, food delivery and beauty products.

The most recent rollout in the region was the launch of GoTo’s GoPayLater Cicil service in August. GoPayLater Cicil is a pay-later service on Tokopedia that enables users on Indonesia’s leading marketplace to split lump sum payments for purchases into monthly installments over one, three, six or 12 months.

The service is currently available to select users at the moment, and adds to the GoPayLater service, which the firm launched in October 2021 and allows users to delay payments until the end of the month.

Compared to other regions, APAC has been found to be ahead of the curve with BNPL. A separate 2022 Mastercard survey found that 50% of APAC consumers are comfortable using BNPL today, a proportion that stands at 41% globally. Looking ahead, the study found that 55% of respondents in APAC said they are likely to use BNPL in the next year.

But the rise of BNPL in Southeast Asia is also prompting concerns over consumer debt and overspending, pushing regulators to introduce rules to ensure fairness and transparency in the sector.

In Malaysia, a task force led by the Ministry of Finance, Bank Negara Malaysia, and Securities Commission Malaysia, is working on a new act to regulate and consolidate all credit activities under one umbrella, including BNPL.

In Singapore, a working group formed by the Singapore Fintech Association (SFA) has developed a code of conduct for BNPL providers aimed at protecting consumers from over-indebtedness and ensuring ethical practices in the industry.

The new code, which was unveiled on October 21, lays out guidelines and best practices for BNPL providers. These include permitting customers to accumulate no more than S$2,000 in outstanding payments at any given time, unless they complete an additional credit assessment. This additional credit assessment must consider, among others, a customer’s income information, and credit information shared across all BNPL firms.

BNPL providers shall also suspend a consumer’s access and use of their BNPL services if they fail to meet any payment obligations.

Providers must be fair and transparent when it comes to their fees. For example, BNPL firms shall cap all their fees, including late fees and other charges, and not charge compounding interest. Fee disclosures must be made to customers in a clear manner.

Apart from creditworthiness safeguards as well as fair and transparent fees, the code also includes guidelines in areas like ethical marketing practices, allowing consumers to easily exclude themselves from BNPL services and promotional materials, and providing hardship assistance to consumers facing financial hardships.