New Report Emphasizes Importance of Fintech in Improving Financial Inclusion

by Fintech News Singapore October 5, 2017Fintech has the potential to dramatically improve financial inclusion, according to a report by the Brookings Institution, an American research group. Incumbents, new entrants, government agencies and policymakers must collaborate in order to harness the full potential of fintech.

The Brookings Financial and Digital Inclusion Project Report, which has been released every year since 2014, aims to provide policymakers, private sector entities, representatives of non-governmental organizations, and the public with information that can help improve financial inclusion in their respective countries and beyond.

The Brookings Financial and Digital Inclusion Project Report, which has been released every year since 2014, aims to provide policymakers, private sector entities, representatives of non-governmental organizations, and the public with information that can help improve financial inclusion in their respective countries and beyond.

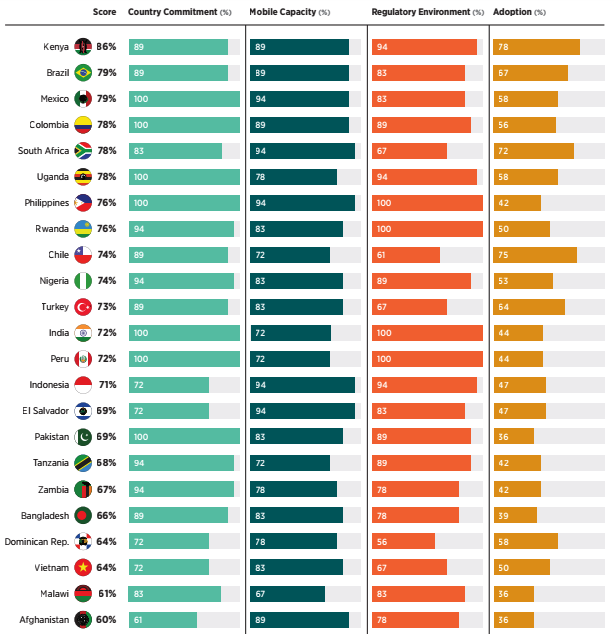

The report valuates access to and usage of affordable financial services by underserved people across 26 geographically, politically, and economically diverse countries. It assesses these countries’ financial inclusion ecosystems based on four dimensions: country commitment, mobile capacity, regulatory environment, and adoption of traditional and digital financial services.

Amongst the 2017 report overall key findings, the organization says that there has been a growing national-level recognition amongst countries that financial inclusion is a key ingredient for sustainable development.

Furthermore, it says that fintech has tremendous potential to accelerate progress toward financial inclusion. But the report also advises countries to amplify investments in cybersecurity efforts and knowledge-sharing in order to fully reap the benefits of fintech innovation.

“The potential benefits of leveraging technology in the financial services sector include reducing costs, enhancing opportunities to meet customers’ evolving needs with new financial service offerings and platforms, and streamlining operations and speeding processes,” the documents reads.

Based on these findings, the report details several possible next steps and recommendations for advancing financial inclusion.

In particular, it advises governments to establish national-level financial inclusion entities and introduce measurable targets related to financial inclusion progress. These entities should establish specific financial consumer protection guidelines.

It also calls for more collaboration between financial inclusion stakeholders such as financial services providers, civil society entities and government entities.

“This dialogue will enable countries to identify promising financial inclusion-related interventions and share key learnings regarding best practices for advancing access to and usage of quality, affordable financial services,” the report says.

To harness the full potential of fintech, traditional financial institutions and fintech companies should coordinate closely and leverage the strengths of each sector. But more importantly, policymakers and regulators should support the growth fintech.

One possible measure could be to establish a regulatory sandbox, similarly to what regulators in the UK, Singapore and Malaysia have also done, to allow firms and startups to experiment with new products and business models “within a supportive and clear regulatory environment.”

But the growth of fintech and digital financial services also brings forward the issue of cybersecurity.

“Policymakers and regulators, fintech firms, civil society entities with financial inclusion expertise, and traditional financial institutions such as banks should amplify discussions surrounding cybersecurity in order to facilitate technical assistance and identify best practices,” the report says. “Financial service providers and entities that house financial data should invest in bolstering the security of outdated or centralized systems in order to protect the integrity of the financial ecosystem.”

For the third year in a row, Kenya ranks at the top of the scorecard, driven by the country’s robust commitment to advancing financial inclusion, widespread adoption of mobile money services, increasing broad rage of mobile-based services, and its enabling regulatory environment for digital financial services.

In addition to Kenya, the other top-scoring countries were distributed across Latin America and Sub-Saharan Africa and include Brazil, Mexico, Colombia, South Africa and Uganda.

These are followed by the Philippines. The organization expects to see other countries in Asia to continue to enhance their digital ecosystems and adoption rates often time given the region’s robust technology environment and widespread adoption of mobile phones.

The report notes the Philippines’s strong country commitment to financial inclusion, its favorable regulatory environment and its mobile capacity.