How Past Lessons in Digital Payments Can Help Banks Navigate in the New Normal

by Wissam Khoury, Finastra May 22, 2020The past couple of decades have seen a complete upheaval in where we buy things and how we pay for them. New technologies have led to huge shifts in consumer behavior and expectation, while businesses have benefitted from faster and more efficient processes.

Today, with physical businesses closed and much of the world’s population still being asked to stay at home, we find ourselves in an unprecedented situation. As a result, the growing acceptance and adoption of digital payments – a trend which was already strong in APAC – has seen years of progression in a matter of months.

As we look towards an uncertain future, it is useful to reflect on the journey so far to look at the challenges those in the payments space have, are, and might face – and how they can overcome them.

Milestones in Consumer Payments

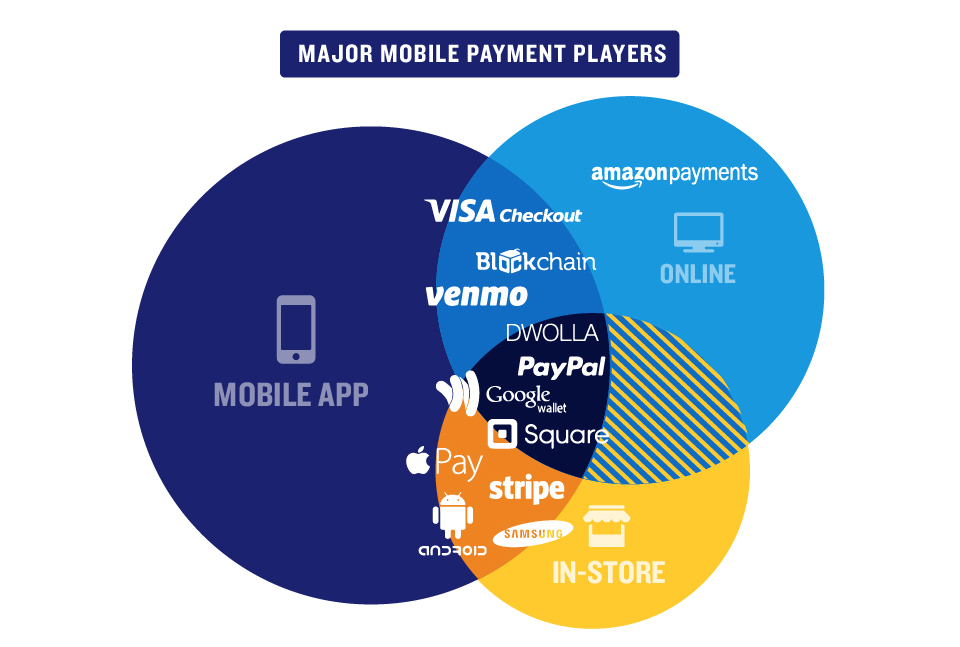

The first decade of the new millennium saw a boom in online payments, with companies like Amazon, eBay and PayPal managing to build payments experiences that were relatively frictionless, as well as demonstrating that online payments were secure.

The decade that followed was the era of mobile. Apple released the first iPhone in 2007, firing the starting gun on a race for innovation and new business models that has been as fast as it has impactful. Mobile payment options began to emerge and Google wallet was introduced in 2011, offering consumers the ability to store and pay with credit cards on a mobile device.

Apple responded with Apple Pay in 2014 and the number of global mobile payments skyrocketed, surpassing desktop transactions for the first time.

image credit: VISA

Mobile also created a platform for a new generation of technology companies that would benefit from APAC’s high rates of smartphone penetration and high numbers of people who are unbanked or underbanked. By focusing on customer service and user experience, as well as being able to offer access to payments services to those neglected by traditional finance, these players have taken banks by surprise and acquired significant amounts of customers in a short space of time.

This has led to a significant lesson for incumbent banks – the value of fintech collaboration. Big banks need to offer more innovative payments services to customers in order to compete with digital challengers. However, the incumbents are often hampered by legacy infrastructure, whereas the challengers are digitally native, agile, and often able to focus on doing one thing really well. By partnering with agile fintech developers, big banks have been able to bring new services to market quickly, avoiding the costs and long lead times involved in developing capabilities themselves.

The Challenges for Business

Businesses have faced similar challenges to banks. While digital solutions offer the chance to do things better and offer new revenue streams, they must also deal with existing processes. Many businesses are still accommodating several payment channels, each with an independent system and workflow. The lack of visibility between these channels can create bottlenecks in the process, often challenging an organization’s cash flow.

Even with digital payments, it isn’t uncommon for payments to arrive separately from remittance information, requiring manual matching. Inefficiencies like this can create friction, making it difficult to determine when a payment has been made and to track overdue invoices. Time spent resolving these issues can lead to high costs for businesses.

With businesses expected to process many more electronic payments in future, it is important they work with technology providers that can help them implement high rates of straight-through processing (STP). This automated process allows the entire payment process, from initiation to final settlement, to be free of human intervention, greatly reducing error and cost.

Another significant challenge for businesses is ensuring that all payment processes work together. Without a seamless relay of information, delays in processing can result as well as a lack of transparency that inhibits efficiency. There is also a continued reliance on paper invoices, despite the availability of technologies that allow for digitization of the payments. Businesses spend many hours per week on paper-based processes, such as investigating invoice exceptions, discrepancies and errors.

Emerging technology

Fortunately, advanced technologies are leading to solutions that can help banks support business customers with the tools they need for seamless, efficient accounts receivables and accounts payables processes.

For instance, Robotic Process Automation (RPA) is a form of automation technology, leveraging artificial intelligence and machine learning, that can perform simple, repeatable human tasks faster and with fewer errors. With payments, RPA can rapidly extract data from invoices or account details. Reducing the need for manual entry not only speeds the process but also reduces the risk of error. This will also benefit businesses by capturing data from various channels and integrating legacy payment systems and core banking environments to automate the entire payment lifecycle.

The next decade will also be more secure, as consumers and businesses alike strike back against cybercrime and identity theft. Biometric authentication, which is already ubiquitous on smartphones and has been tested in physical retail settings, has the potential to replace frustrating and time-consuming multi-factor authentication processes by the decade’s end, securing financial data and systems for a more integrated and safe payment tomorrow.

Payments in the new normal

As we move into a future where even more people are using digital payments and the use of cash declines even further, consumers can expect to have greater choices of payment method. They will be able to choose based on ease-of-use, their cash flow management needs, credit accessibility and rewards programs. Artificial Intelligence will help consumers decide which option will work best for them at that point in time. The only question is how quickly banks will react to the new normal in the face of agile, specialized digital challengers.

Featured image credit: Business photo created by master1305 – www.freepik.com