Southeast Asia Becomes Centre for Instant Cross-Border Payments Growth

by Fintech News Singapore September 25, 2020Following in the footsteps of the European Union, ASEAN is moving towards having its very own Single European Payments Area (SEPA)-style payments network, making Southeast Asia a global focal point for cross-border real-time payments growth, according to a new report by ACI Worldwide and fintech market research and consulting firm Kapronasia.

The research, titled Envisioning a pan-regional real-time payment ecosystem in Southeast Asia, looks into the real-time payments landscape across Southeast Asia and the broader Asia Pacific (APAC) region, and delves into the different national payments networks currently in operation.

The real-time payments landscape in Southeast Asia

The past decade has seen economies across APAC modernize their payments systems, replacing their domestic infrastructure to make payments cheaper, faster, and more efficient.

Southeast Asia in particular has been making strides in terms of innovation in real-time payments with many regulators launching tools including instant payments, QR codes, and real-time direct-debit networks.

Singapore launched its Fast And Secure Transfers (FAST) real-time electronic fund transfer service in 2014, allowing individuals and entities alike to conduct electronic transfers in real-time. FAST is operated by the Network for Electronic Transfers (NETS), an electronic payments service provider owned by DBS Bank, OCBC Bank and United Overseas Bank (UOB).

Malaysia introduced the Real-time Retail Payment Platform (RPP) in early 2019 after a multi-year effort to modernize its infrastructure. Payments Network Malaysia (PayNet), which operates the RPP, envisions the platform as one of the pieces in enabling cross-border instant credits and peer-to-peer (P2P) payments across the ASEAN region, PayNet group CEO Peter Schiesser, said in January 2019. Bank Negara Malaysia (BNM) is PayNet’s single largest shareholder with eleven Malaysian financial institutions.

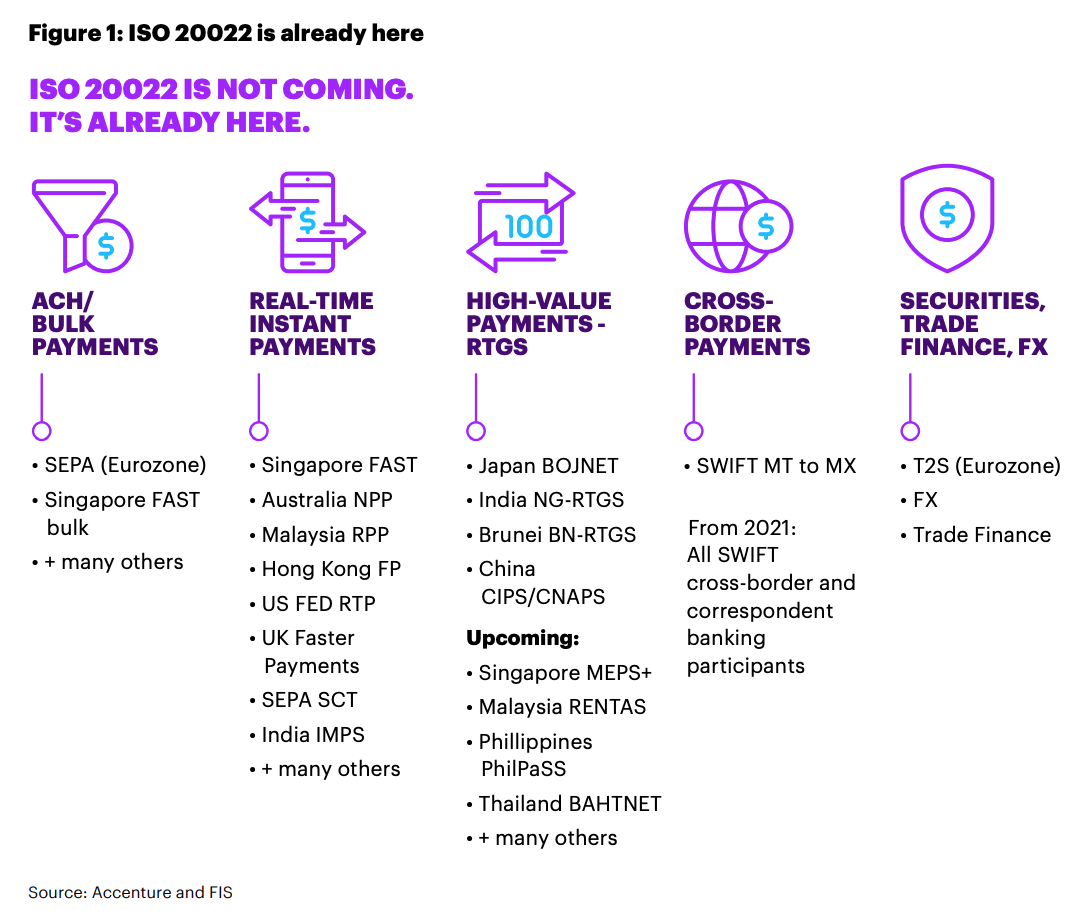

ISO 20022 is already here, ISO 20022: The Challenges and Opportunities for APAC’s Financial Institutions, Accenture, 2019

Linking domestic real-time payments infrastructures

Although these projects have been mainly focused on their respective domestic markets, Southeast Asian countries are making efforts to create cross-border linkages, inking a number of biliteral and multi-lateral arrangements.

Such arrangements include for example the memorandum of understanding (MoU) signed between Southeast Asian payments system operators NETS, PayNet, as well as National ITMX (ITMX) of Thailand, National Payment Corporation of Vietnam (NAPAS) and PT Rintis Sejahtera (Rintis) of Indonesia, to enable real-time cross-border payments by connecting their respective payments infrastructures.

These operators are members of the Asian Payment Network (APN), an initiative launched in 2006 to function like SEPA. As originally envisioned, the APN would begin in the ASEAN countries and eventually grow to include more nations across APAC.

Another example is the linkage of Singapore’s PayNow, the peer-to-peer (P2P) fund transfer service launched by the Association of Banks in Singapore (ABS) in 2017, to Thailand’s equivalent service, PromptPay. It was announced earlier this year that the cross-border link between Singapore and Thailand will be extended to Malaysia’s DuitNow, an instant fund transfer platform.

In Malaysia and Singapore, their respective payments system operators, PayNet and NETS, officially launched real-time, cross-border debit card payments in late-2019, making usage of Singapore’s NETS ATM cards possible in Malaysia and usage of Malaysia’s MyDebit ATM cards possible in Singapore.

NETS and PayNet have since been working on connecting their respective real-time payment infrastructures to enable cross-border instant fund transfers and QR payments between Singapore and Malaysia.

QR code payments interoperability is also an area that jurisdictions including Thailand and Cambodia have been pursuing. Regulators from the two countries announced in February 2020 that they were working on a QR code payments initiative that would allow tourists from their respective countries to pay using a mobile app in the other country.

Given all the recent developments being made across ASEAN, it’s likely that real-time, cross-border payments will first become a reality in Southeast Asia before other markets part of the APN, the report says.

“Southeast Asian countries are making significant strides in payments modernization, with nearly every major country in the region having robust domestic real-time payments infrastructure in place,” Leslie Choo, managing director for Asia at ACI Worldwide, said in a statement. “Despite the lack of uniform regulations and disparate economic priorities across the region, it’s clear that market forces — driven by the needs of businesses and consumers — will propel Southeast Asia towards the realization of a multi-country real-time network.”

Featured image credit: Unsplash