Has the Southeast Asian startup ecosystem ever witnessed a quarter more exciting than the current one?

We entered the second quarter with Grab’s blockbuster SPAC listing. Valuing the super-app at US$40 billion and being the largest SPAC deal to date, it placed Southeast Asia into the global spotlight.

As the dust settled on news of the region’s first tech listing in the US since Sea Group, Gojek and Tokopedia thrust the ecosystem back into the spotlight by officially announcing they were merging to form GoTo Group.

While financial details regarding the combined entity were not disclosed, the press statement noted Gojek and Tokopedia will continue operating as separate entities.

A new financial services arm, GoTo Financial, will be created and headed by Andre Soelistyo, who is also the Group CEO. Soelistyo was previously CEO of GoPay, which headlines the suite of financial services operated under the new entity.

(L-R) Kevin Aluwi and Andre Soelistyo Image Credit: Gojek

Other services include GoSure (insurance), GoInvestasti (investments), Paylater (a buy now, pay later service), Midtrans (payment gateway) and Moka (point-of-sale).

The creation of a standalone entity to oversee financial services shows its strategic importance to the Group. Fellow tech giants Sea and Grab have created independent financial entities with SeaMoney and Grab Financial Group respectively. Therefore, GoTo’s move should come as no surprise with fintech shaping up to be a key growth lever for tech companies.

Is GoTo SEA’s answer to Alibaba?

Image credit: Alibaba

By joining forces, the scale of GoTo’s operations is immense.

The Group claims it has a total gross transaction value (GTV) of US$22 billion and more than 100 million monthly active users (MAU), creating a digital ecosystem encompassing two per cent of Indonesia’s GDP.

The all-encompassing nature of GoTo’s ecosystem makes it a fertile ground for providing digital financial services, as seen from Ant’s success in China.

An affiliate company under the Alibaba Group, Ant has leveraged the latter’s digital ecosystem to supercharge its growth. Besides the B2C e-commerce platform Taobao, Alibaba also has 1688 (B2B e-commerce) and Freshippo (grocery commerce) within its portfolio.

As such, Ant’s digital wallet platform AliPay boasts over 1 billion users and processed US$16 trillion in transactions in 2019.

The data generated by users on the Alibaba ecosystem – from transaction histories on Taobao to merchant orders on 1688 – forms the backbone of Ant’s success. Besides allowing the company to personalise financial offerings to the needs of individual users, it also enables Ant to collect a wealth of data to power credit scoring and underwriting requirements of their products.

This allows Alibaba users to easily access the suite of financial services provided by Ant. Borrowers can complete their loan applications within three minutes due to the depth of information Ant has on them.

While not on the scale of Alibaba, GoTo creates a similar high touchpoint ecosystem by providing a range of services including ride-hailing and e-commerce. Besides, the Group also provides food delivery and entertainment options.

Therefore, the prevalence of the Group’s platform within a consumer’s daily life provides GoTo Financial with a plethora of data on the financial needs of their users. Besides building a more comprehensive credit scoring system, it also enables the company to tailor its services to the specific needs of its users.

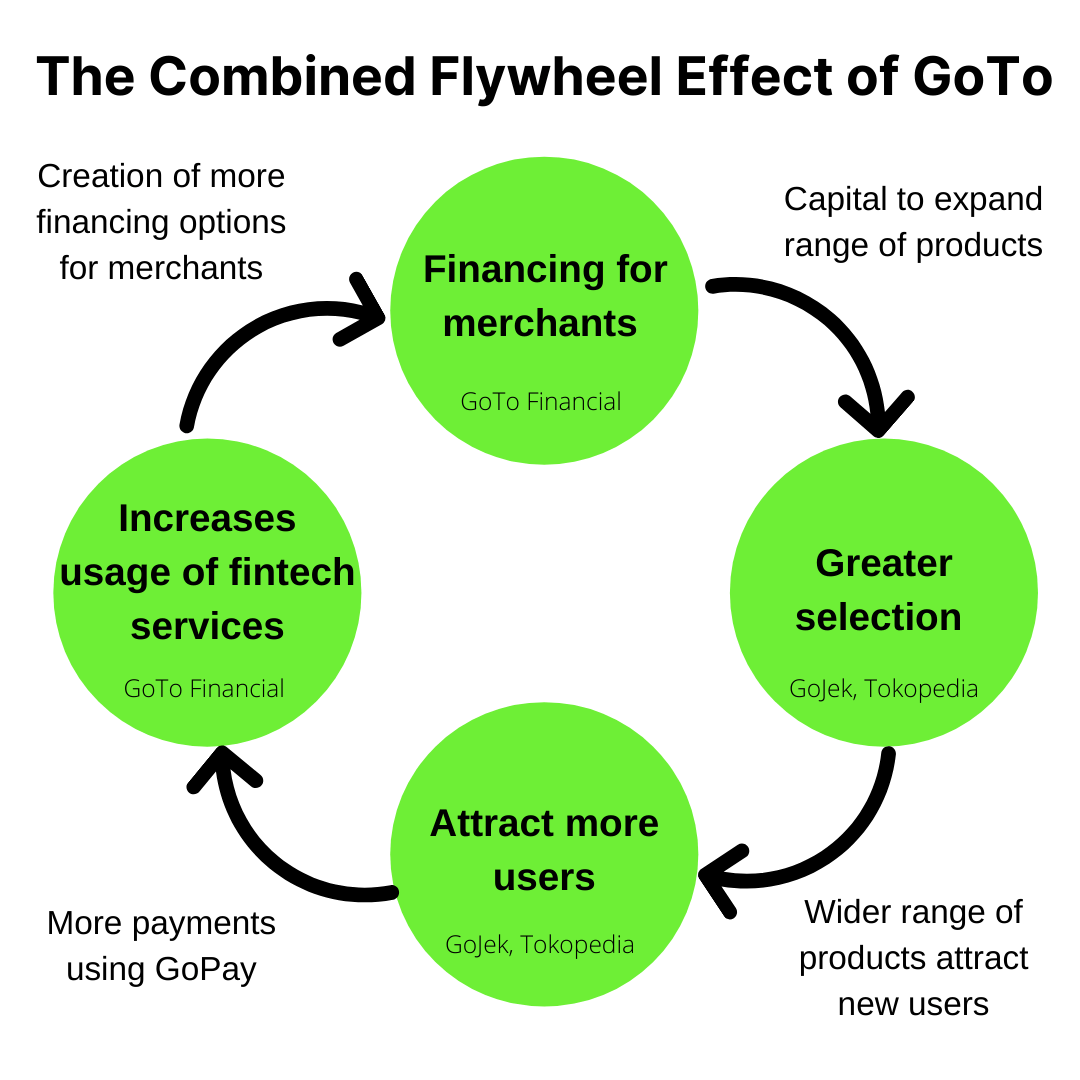

Flywheel effect

The relationship between Gojek, Tokopedia and GoTo Financial is mutually beneficial. The provision of financial services creates a flywheel effect that drives growth for the rest.

For instance, through an accelerated credit scoring process, GoTo Financial can issue more loans to merchants on both platforms.

With increased access to capital, merchants can either expand their product range or improve the quality of their offerings. This attracts new consumers to the platform, driving growth in transactions that would occur through GoPay.

Consequently, the growth in GoPay will fuel the creation of more financing options for merchants, allowing the cycle to repeat. This creates network effects for the Group while boasting its moat.

The synergies within GoTo. Illustration by Tun Yong Yap.

Digital banking

Indonesia’s high unbanked population would see digital banking play a key strategic role for GoTo.

The World Bank estimates 95 million Indonesians, one-third of the country’s population, do not have bank accounts. However, of that 95 million, 60 million own a mobile phone, representing a large untapped market to offer digital banking services for.

Recognising this opportunity, Gojek currently owns 22 per cent of Bank Jago, which has dubbed itself as Indonesia’s first digital bank. Integrating Bank Jago into the GoTo ecosystem would allow the former to offer banking services for the latter’s 100 million users, a significant proportion of which is unbanked.

Payments battle royale

In comments accompanying the merger announcement, Patrick Cao, President of Tokopedia, noted the e-commerce platform is looking to divest its stake in digital payments platform Ovo.

With its hands tied by Bank Indonesia’s single presence policy prohibiting companies from holding a controlling stake in more than one licensed payment provider, Tokopedia would have to divest its stake in Ovo to ensure GoPay can continue operating under GoTo.

Currently, the most plausible solution is the sale of its 41 per cent stake to Grab. Besides, Grab Financial Group has the dry powder for this transaction to take place. In January, the financial services arm raised US$300 million in fresh capital.

With a majority stake in Ovo, Grab could look to merge it with Dana and create a payments powerhouse. Grab has been building an alliance with Emtek, the Indonesian conglomerate that owns Dana. Grab purchased a 4 per cent stake in Emtek last month with the latter acquiring a minority stake in the former’s Indonesian unit last week.

This sets up a battle royale within the Indonesian payments industry, with a potential Ovo-Dana entity coming up against GoPay and Sea’s ShopeePay.

A recent survey by market research firm Snapcart revealed ShopeePay was the category leader, with 76 per cent of respondents using it. This was followed by GoPay (57 per cent), Ovo (54 per cent) and Dana (49 per cent).

The current pecking order could change with Ovo’s loss of Tokopedia’s users and GoTo’s combined might. ShopeePay would also have to contend with GoPay’s access to the behemoth GoTo ecosystem.

Selling the vision

GoTo has created a super-app unlike any within Southeast Asia. By embedding financial services within its ecosystem, we are seeing a replication of Alibaba’s strategy within the region – albeit on a smaller scale.

That could well be the narrative GoTo sells to investors as it embarks on pre-IPO fundraising, with the Group seeking a post-money valuation of US$40 billion. This is more than double the current combined valuation of Gojek (US$10.5 billion) and Tokopedia (US$7.5 billion).

As GoTo lines up a domestic and international listing, the influx of capital would arm it with the capital firepower to acquire fintechs within Southeast Asia. This allows the Group to build on its super-app strategy, taking it one step closer to its goal of building the region’s Alibaba.