IMF: Despite the Hype, Fintech Has Yet to Disrupt the Remittance Market

by Fintech News Singapore January 12, 2023Despite enthusiasm surrounding the potential of fintech to disrupt the remittance market, evidence shows that there is a gap between the hype and the reality on the ground. In fact, and contrary to expectations, fintech companies are increasingly being entangled with incumbents and partnering with money transfer operators and banks to tap into their extensive non-digital footprints, a new paper by the International Monetary Fund (IMF) says.

In a working paper, titled Curb Your Enthusiasm: The Fintech Hype Meets Reality in the Remittances Market, the IMF looks at the fintech landscape in the remittances market and investigates whether new digital players have had a disruptive effect on cross-border transactions.

The paper argues that while data show that remittance technology (remtech) providers and mobile money remittances are, on average, cheaper than traditional remittance service providers, including money transfer operators and banks, there are no signs that these new market entrants have disrupted, or are disrupting, the remittance market.

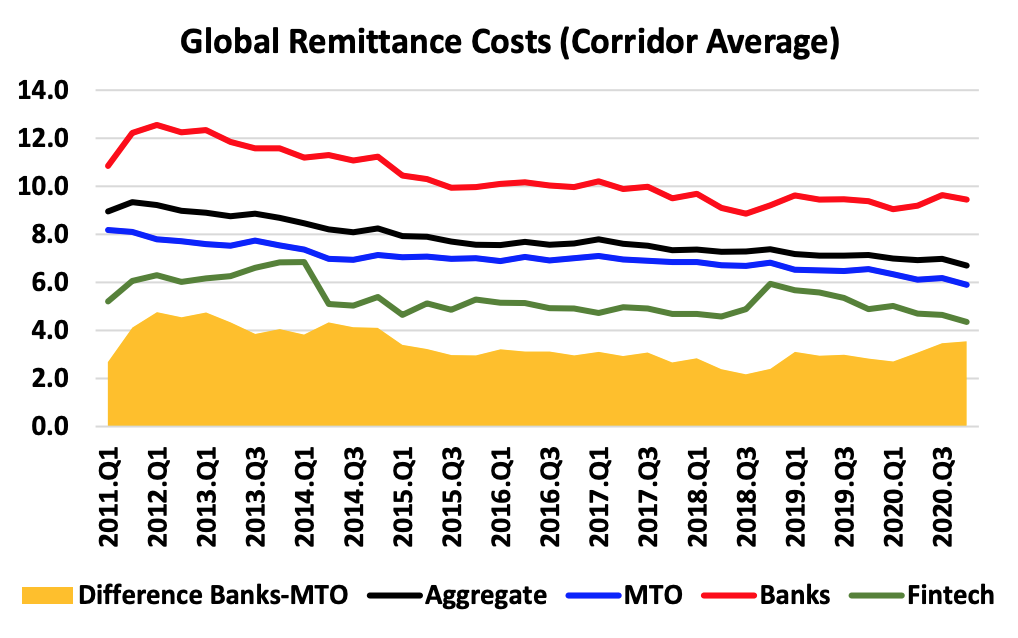

Global remittance costs (corridor average), Source: IMF Working Paper, Dec 2022

Remtech companies operate under innovative digital business models, the paper notes, and while these business models enable a smaller footprint and more convenience, they also prevent them from disrupting the remittances market. This is because most remittances still involve cash, a structural factor which impedes digital disruption.

In addition, many remtech companies have partnered with banks and money transfer operators to gain scale and expand, showcasing that, in order to grow, these companies not only need the large non-digital footprint of the incumbents, but also their payments infrastructure. This shows that instead of disrupting traditional remittance service providers have actually become increasingly entangled with them.

It also explains why remtech companies have shown a clear preference for entering richer and larger corridors where their business models are more tailored to, instead of entering smaller corridors in markets in real need of disruption.

In addition to remtech, the IMF paper also analyzes two other materializations of fintech that have been praised for their potential to disrupt the remittance market: Bitcoin and mobile money.

According to the paper, while Bitcoin and its technological backbone, the blockchain, have been touted as a game changer for remittances, several important aspects of these technologies have been overlooked, including costs. Since most remittances are sent and received in cash, sending money across borders through cryptocurrencies implies extra transaction costs, in addition to the regular network fees. This makes cryptocurrencies ill-suited for remittances, the paper says. A testament of that is the fact that use of bitcoin remittances is virtual non-existent, it notes.

Mobile money, meanwhile, has played a critical role in improving financial inclusion in a number of emerging markets. However, one of the key factors behind the success of services like Kenya’s M-Pesa is the large physical footprint of agents these players rely on. This means that the success of digitalisation through mobile money largely depends on establishing a large non-digital footprint, the paper says. It adds also that even in countries where mobile money is popular, its use for international transactions remains marginal.

Although evidence shows that fintech has yet to disrupt the remittance market, new market entrants have played an important role in fostering competition, driving costs down and pushing incumbents to improve the quality and convenience of their services, the paper says.

The global digital remittance market was valued at US$18.16 billion in 2022, according to American market research firm Fact.MR. Within the next decade, the market is expected to grow at a compound annual growth rate (CAGR) of 13.5% to reach US$64.43 billion by 2032. This growth will be driven by rising penetration of mobile devices and increasing number of cross-border transactions.

In 2022, global remittance flows increased by 1.7%, to reach US$794 billion, according to the latest World Bank Migration and Development Brief. Much of this amount went towards low- and middle-income countries, which received a total US$626 billion.

In low- and middle-income countries, remittances are a vital source of household income, helping reduce poverty, improve nutritional outcomes and having been associated with higher school enrollment rates for children in disadvantaged households.

Featured image credit: flickr