Why Risk-Averse Southeast Asian Banks Should Embrace a ‘Multicore’ Approach

by Fintech News Singapore January 26, 2022The banking industry is in the midst of a period of intense transformation in Southeast Asia, and indeed the world, driven in part by the pandemic, but also influenced heavily by changing consumer demand and fast-moving technological innovation.

Predicting the future of banking, while never an easy task, is now more uncertain than ever, with new trends emerging regularly and regulatory changes occurring at pace.

To get a clearer understanding of how Southeast Asian banks view the future of core banking within their organisations, IDC Financial Insights interviewed a number of Southeast Asian banking executives, discussing their thoughts on legacy core banking, the risks associated with transformation, and how they plan to capitalise on the benefits that digital banking can deliver.

The white paper “Leveraging Digital Core Banking Systems: Next-Level Banking” found that Southeast Asian banks want to be able to use a combined legacy and digital core banking approach to succeed in the new era of banking which is known as the ‘multicore’ approach.

Key findings of the research

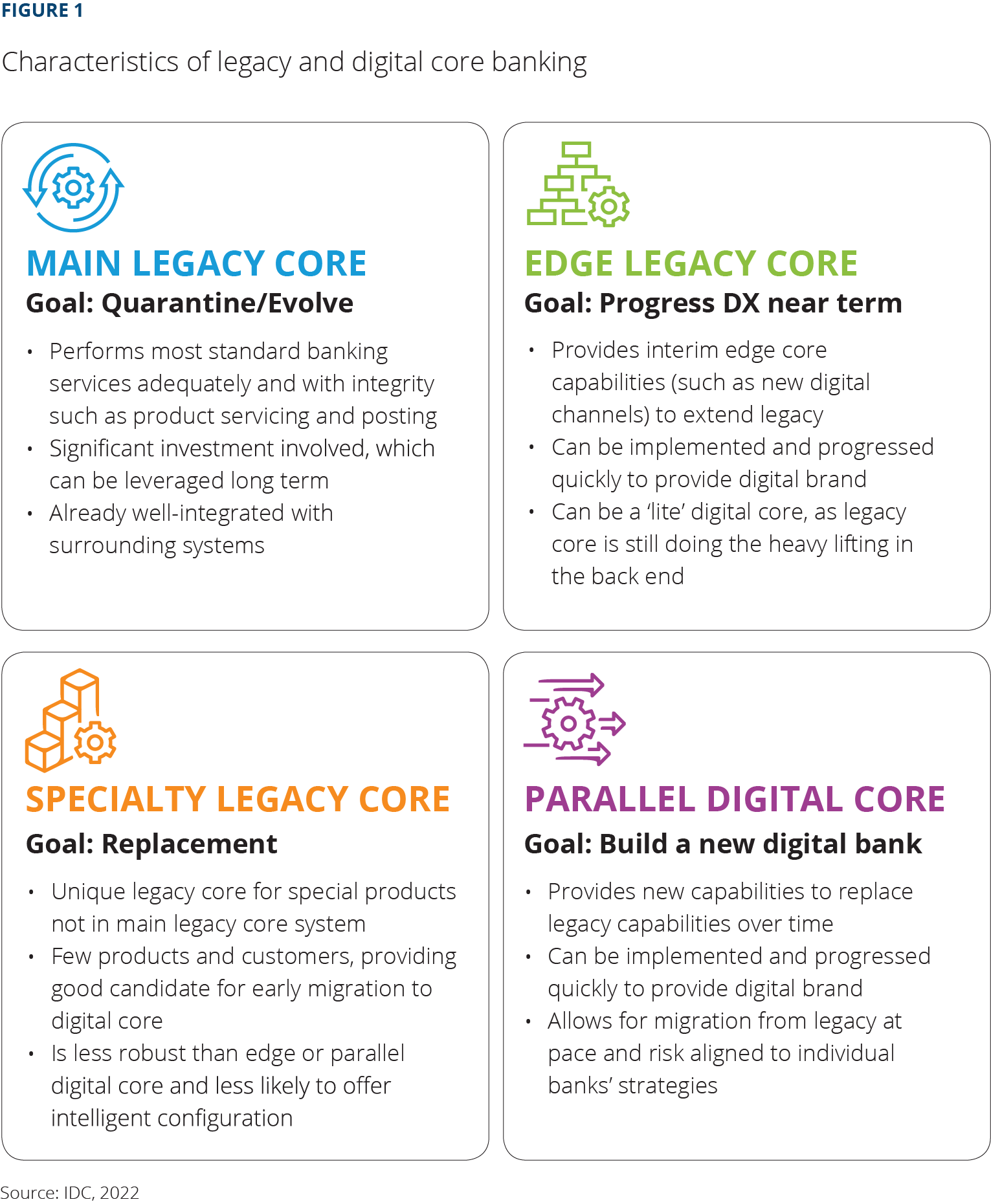

- The challenge for established banks in Southeast Asia, many of which have core banking systems that are already 20 years old or more, is to deliver on the promise of digital banking without exhausting their financial resources or risking their reputation

- Southeast Asian banks are often risk-averse and want to extend the value and life of legacy core banking

- Despite this, Southeast Asian banks clearly understand the need for and value of digital banking

The ‘multicore’ approach

The multicore approach to digital transformation could be just the answer that Southeast Asian banks wary of ‘big bang’ style transformation are looking for.

However, it’s important to note that while a multicore approach can certainly extend the life and value of legacy core banking – sometimes considerably – even with this approach banks must have plans in place to eventually migrate to a fully digital core.

The multicore solution should be viewed as a way to stretch out the transformation phase, making smaller changes incrementally rather than doing everything at once.

This ‘softly, softly’ approach seems to appeal particularly to banks in Southeast Asia, where the appetite for risk is low, and rapid change can be seen as a threat.

The multicore approach is an ideal solution for Southeast Asian banks looking to reduce the risk associated with digital transformation, but who also understand that they need to join the digital banking revolution to be able to offer the hyper-personalised and customer-centric experiences that consumers now expect.

Benefits of a ‘multicore’ solution

- Extend the life and value of legacy technology

- Reduce risk – technical, reputational, and financial

- Smoother pathway to digital transformation

Even with a multicore approach, legacy technology must eventually be replaced

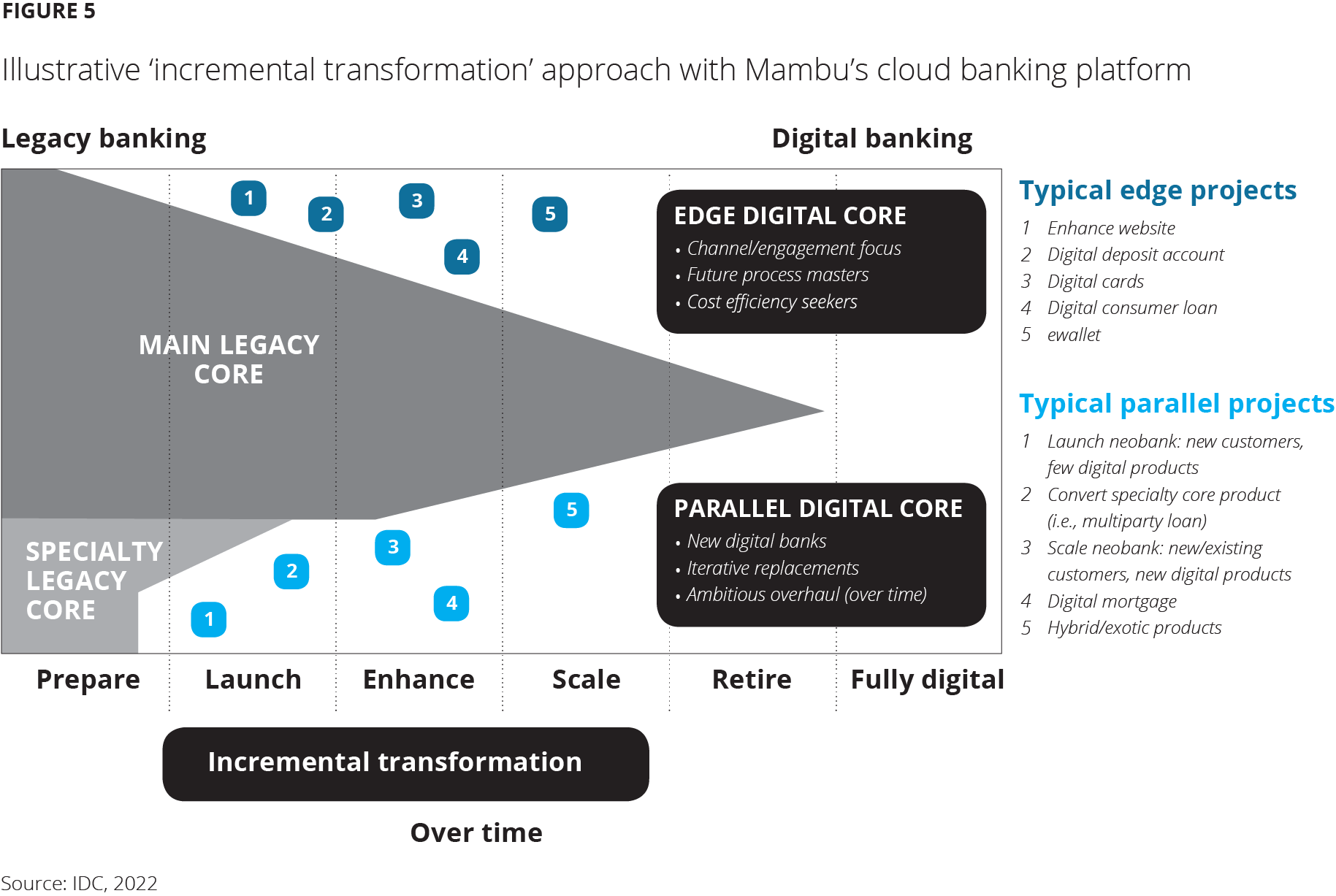

Fortunately for these risk-averse Southeast Asian banks, there is a new breed of digital core banking providers – like Mambu – that are able to deliver a multiple core – aka ‘multicore’ – solution.

The multicore model values the role of legacy core banking well into the future, reducing the potential technical, financial, and reputational risks associated with a ‘rip and replace’ approach to transformation.

Its SaaS cloud banking platform enables easier connection of multiple core systems, which in turn reduces the risk of replacing legacy core and extends its value longer term.

Mambu has helped several Southeast Asian banks on their digital transformation journeys, enabling them to extend the life of their legacy core banking while also embracing the new technologies that their customers now expect.

Download this white paper “Leveraging Digital Core Banking Systems: Next-Level Banking”, sponsored by Mambu, to understand the choices and challenges of incumbent banks faced with legacy core banking systems, and how a new banking model can enable them to become a digitally-enabled bank.