How CIMB and Finhay Are Delivering Diversification Through Embedded Finance in Vietnam

by Fintech News Vietnam May 14, 2021Embedded finance will transform the role of finance, making it contextual, convenient and cost-effective. Instead of finance being a stand-alone function, it will get ingrained into the lifestyle of customers, whether it is making credit available at the point of sale or providing smart advice during a customer’s life event.

And, indeed, we are now seeing the popularity of embedded-finance solutions in the real world. Apple’s collaboration with Goldman Sachs to produce Apple Card gave the tech giant an important financial tool embedded within the Apple ecosystem. In Vietnam, recently, Đoàn Văn Hiểu Em, CEO of the Mobile World’s store chain revealed a plan to develop financial utilities embedded in his system. CEO Danny Le of Masan Group also announced the development of synchronous financial utilities in their WinMart stores after acquiring this system (VinMart) from VinGroup.

Embedded finance isn’t new. The difference now is that the internet enables a fully integrated banking experience on a massive scale. Once this experience is built, it can be infinitely replicated thanks to existing fintech infrastructures.

And now people keep asking : “Why is Embedded Finance So Important?”

It’s not a matter of whether embedded finance will disrupt banks, but when.

Embedded finance is critical because it allows for professional and safe financial operations to be directly inputted into any platform.

The new wave of fintech innovation may come far away from the world of finance. Perhaps the defining shift in consumer finance will be the transition of the Big Four banks and other legacy institutions away from their public-facing role.

Thomson Fam Siew Kat

“For the next generation of consumers, banking will be something that you ‘do’ with your favourite brands rather than your chosen bank”,

said Thomson Fam Siew Kat, CEO of CIMB Vietnam.

“Consumers and businesses will no longer see banking as a separate sphere or sector, and will instead come to expect that day-to-day financial tasks will be carried out within their favourite brand ecosystems. And if you’re a traditional bank, it’s time to start gearing up for a battle of your own—one that isn’t necessarily going to be on home turf”.

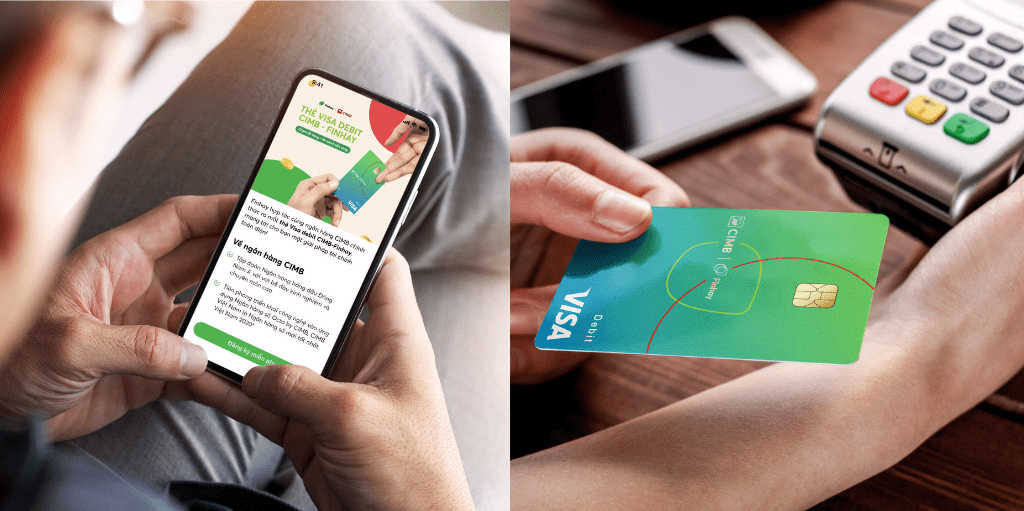

To meet the rising demand for embedded finance, CIMB Vietnam has increasingly offered embedded finance since 2019 — bundled offerings and co branded services that nonbanks can use to serve their customers. With the ambition to drive the new era of modern financial products in Vietnam, in June 2021, CIMB Vietnam partnered with Finhay to launch a co-branded debit card with virtual account. The collaboration between CIMB Bank Vietnam and Finhay – has given birth to the country’s first-ever 3-in 1 bank account that can be opened and maintained straight from the Finhay app.

Trends to watch – Customer demand for integrated experiences

Finhay users will be able to open virtual accounts & co-branded Debit Cards right on Finhay app with eKYC solution by CIMB to Take control with all-in-one spending, saving, investment, and more. With the only spend account and debit card that saves and invests, users can instantly invest, save, Zero fee transfer and withdraw money from no hidden fees with over 17,000 fee-free ATMs nationwide.

Finhay and CIMB customers will now be quickly provided with smart and modern financial – banking solutions, enabling them to plan and optimise the implementation of financial solutions with small amounts from VND50,000 or VND100,000. Smart spending by cards is also consistent with smart financial and consumption trends. It helps customers spend with the smallest amounts.

Nghiem Xuan Huy

Nghiem Xuan Huy, CEO of Finhay said,

“Embedded Finance helps people to seamlessly and easily transfer funds from an account or, frankly, any stored value account into something that is able to get returns in the market. This enabled banking to be built into nearly any industry.

Thanks to partnership with CIMB Vietnam, we now can provide access to bank accounts , fund transfer and lending in the future. I think the sense of market is pretty amazing to watch, I don’t know how long that trend is going to go on, but it’s something that we’re starting to see demand for.”