The travel payments industry is undergoing a profound transformation, driven by the rise of fintech, evolving consumer preferences and changing market dynamics.

A 2023 white paper by Mastercard, titled “Embracing a virtual future of B2B travel payments”, explores these transformations and their impact on the sector.

The paper discusses how the pandemic has triggered a reevaluation of business-to-business (B2B) payment practices, the growing prominence of the merchant of record (MoR) payment model, and the increasing adoption of virtual cards.

Traditionally, travel agencies mainly served as intermediaries, transmitting consumer payment details to various service providers in an individual’s travel itinerary. However, the expanding network of suppliers has made this “pass-through” approach riskier and more cumbersome for both agencies and consumers.

To address these risks, an increasing number of travel agencies are shifting to the MoR model where the travel agency collects customer payments for all booked services, authorizes transactions, and then disburses payments to the specific suppliers associated with the booking.

The MoR model not only addresses these challenges but also opens up new opportunities for suppliers, allowing agencies to offer consumers new payment options such as installment methods and buy now, pay later (BNPL) arrangements.

The report notes a significant migration from the pass-through model to the MoR model, with travel agents acting as MoRs posting a compound annual growth rate (CAGR) of 43% from 2020 to 2022, a growth rate that’s more than double than that of the overall online travel agency market of 20% CAGR.

Another trend outlined by the Mastercard white paper is the digitalization of business-to-business (B2B) travel payments, with virtual cards in particular emerging as an appealing payment option. Virtual cards are essentially digital versions of physical payment cards. Virtual card numbers are digitally generated, PCI-compliant and single-use card numbers that are accepted everywhere traditional payment cards are.

According to Mastercard, virtual cards provide a unique, traceable link between booking and associated payments to third-party suppliers. They allow travel agencies and suppliers to easily track and reconcile payments, while offering benefits such as flexible pricing, financing options and card payment guarantees.

This results in a more streamlined payment experience for travel agencies and their customers, as well as travel suppliers. Transactions are also more secure, with Mastercard data revealing that the risk of fraud is 30 times lower when using virtual cards compared to traditional payment cards.

A 2023 infographic produced by Up in the Air, a travel payment consultancy from the Netherlands, depicts a dynamic and diversified B2B travel payment landscape.

This landscape comprises popular payment card schemes such as Visa, Mastercard and American Express; virtual card issuers such as banks; payment technology companies such as Stripe, Nium and Airwallex; as well as travel payment pure players such as Outpayce, a B2B payments business serving the travel industry, Mystifly, an airfare distribution and payments settlement marketplace platform, and iOL Pay, an automated payment acceptance solutions for the hospitality industry.

Airline and travel payments – B2B vendor landscape 2024, Source: Up in the Air via LinkedIn, Nov 2023

Asia’s travel sector rebounds, though challenges remain

After the COVID-19 pandemic brought the travel and tourism industry to a near standstill, the sector rebounded in 2022 and 2023. Indonesian online travel platform Traveloka posted a 75% increase in revenue for its 2022 financial year and a reduction in losses of 29%. Meanwhile, Google reported that demand for international travel in Asia-Pacific (APAC) skyrocketed to 85% above 2019 levels in 2023, while domestic travel demand surged by 52%.

In Southeast Asia, South Korea and Japan, growth in tourism spending, coupled with cross-border e-commerce, is expected to fuel the estimated US$232.4 billion in additional revenue that businesses in the locations will generate from 2022 to 2027, according to a report by market intelligence firm IDC and commissioned by global payments platform 2C2P and Ant Group.

Mastercard estimates that globally, about 1.5 billion more people booked flights in 2022, compared with 2021, forecasting that online bookings reached pre-pandemic levels last year. According to the payment firm, global leisure travel increased by roughly 31% in March 2023 compared to the same period in 2019, representing an impressive 25% year-over-year-to-date change from 2022 to 2023.

Despite promising growth and prospects for the tourism industry, travel tech still faces challenges, owing to ongoing conflicts around the world, the current economic downturn and intense competition in the online travel industry. Noteworthily, Indonesian online travel agent Pegipegi ceased operations in December 2023 after 12 years of service, Dinsights reported.

At the same time, venture funding to the sector has declined substantially. Since fundraising hit a peak in 2021, Asian travel tech startups have recorded an over tenfold decline in the total funds raised in 2023, while deal count decreasing by over 60%.

This trend is reflective of the global fundraising downturn. In the first ten months of 2023, worldwide travel and tourism funding deals contracted by 31.8% year-over-year, with APAC experiencing an 11.7% decrease over the same period, research conducted by GlobalData show.

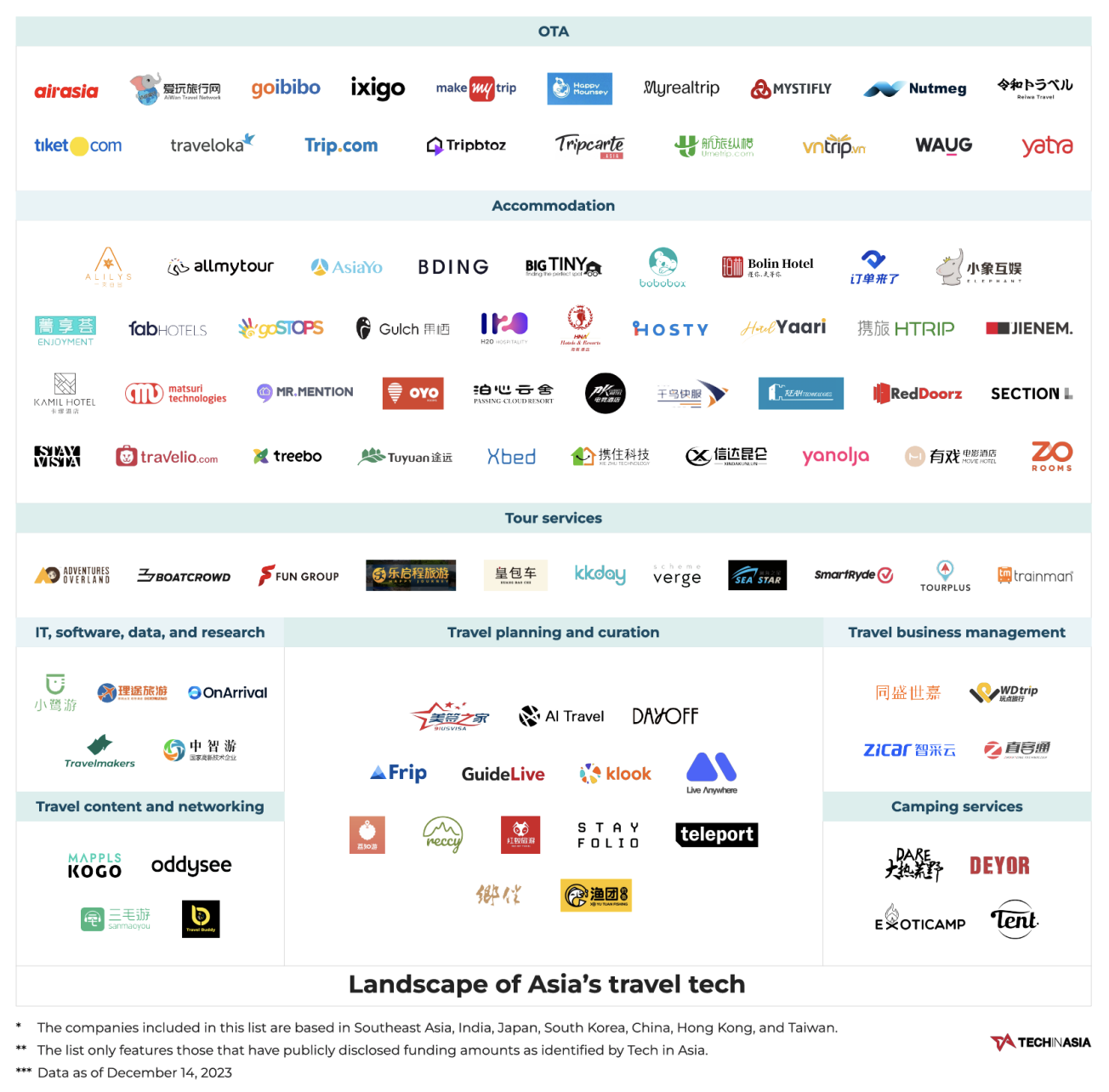

Landscape of Asia’s travel tech sector, Source: Tech in Asia, Dec 2023